Strategy’s Preferred Stock Complex: Institutional Credit Analysis of STRF, STRC, STRE, STRK and STRD

Executive thesis

Strategy’s preferred instruments should be analyzed less like ordinary corporate preferred shares and more like structured claims on a Bitcoin treasury balance sheet. They sit above common equity but below debt, depend heavily on the market value and liquidity of Strategy’s Bitcoin holdings, and are supported in the near term by the company’s USD reserve. They offer high stated income because investors are accepting exposure to BTC price volatility, capital-market access risk, preferred issuance risk, and board-level dividend discretion.

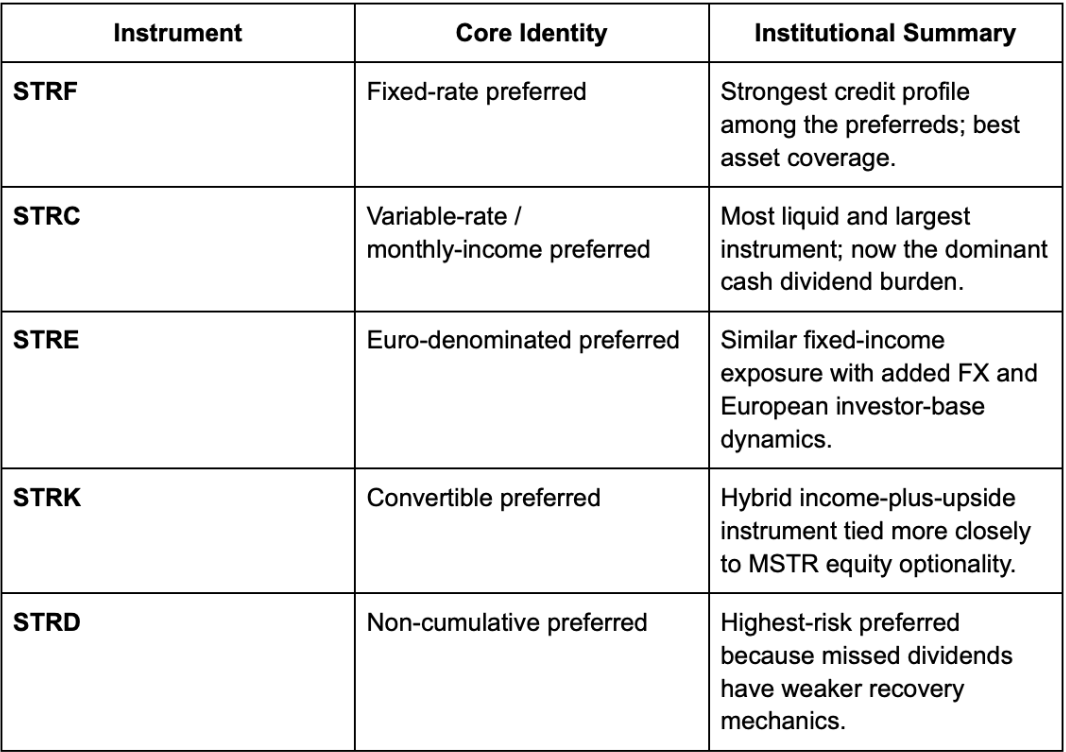

The current preferred complex consists of five listed instruments:

The cleanest credit instrument is STRF. The best liquidity and income instrument is STRC. The best upside-oriented instrument is STRK. The weakest from a conservative credit perspective is STRD.

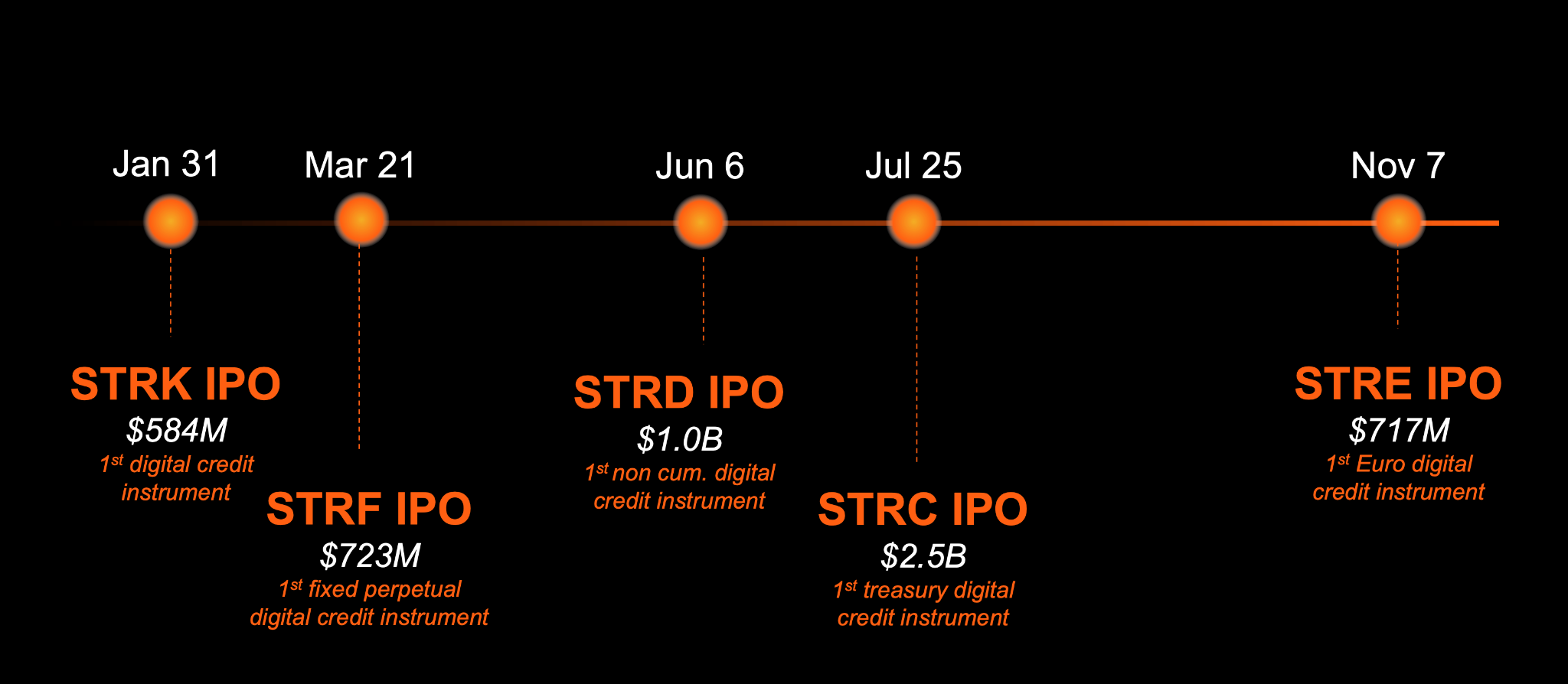

Preferred issuance timeline

Figure 1: Strategy preferred instrument issuance timeline. Strategy’s preferred complex was built in stages during 2025. STRK came first on January 31, followed by STRF on March 21, STRD on June 6, STRC on July 25, and STRE on November 7. This sequencing is important because each instrument was designed to target a different investor base: STRK for upside participation, STRF for fixed perpetual income, STRD for high-yield non-cumulative exposure, STRC for treasury-style monthly income, and STRE for euro-denominated credit exposure.

Capital structure: where the preferreds actually sit

The critical starting point is that Strategy preferred stock is not debt. The base prospectus states that preferred stock ranks senior to common stock but is subordinate to Strategy’s creditors. Dividends are payable only when, as and if declared by the board. That distinction matters: even cumulative preferred dividends are not the same as contractual debt interest.

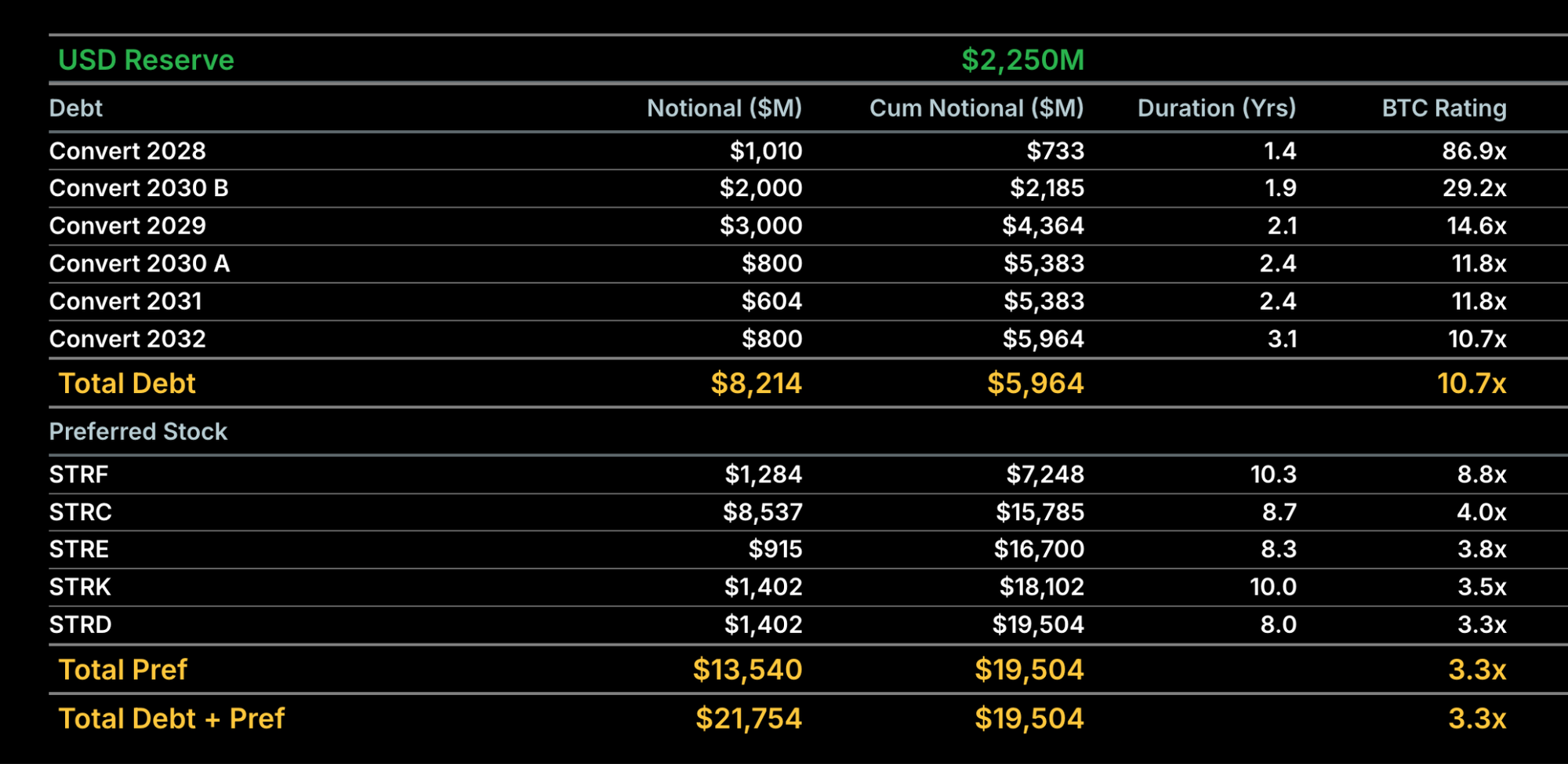

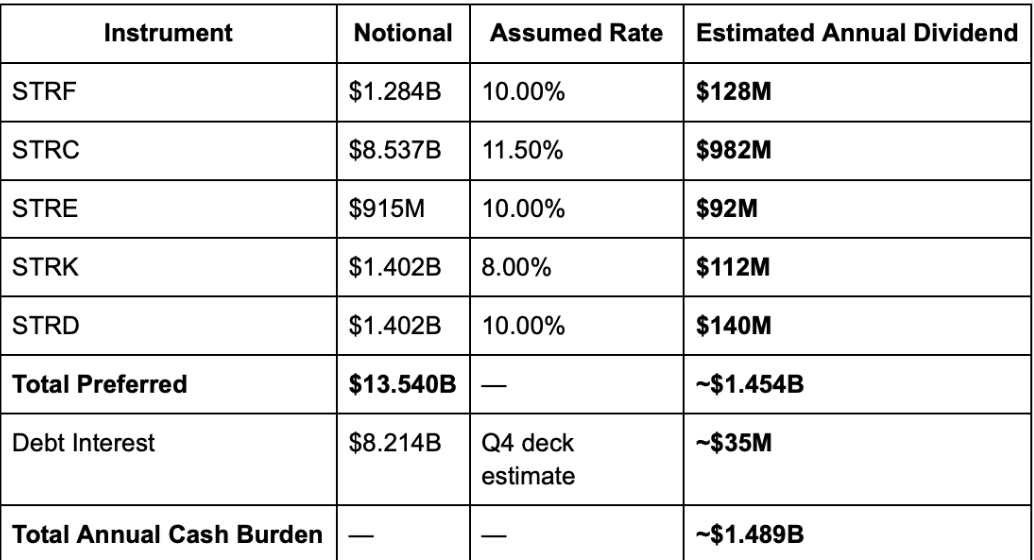

Latest uploaded capital-stack image as the most current data, the structure is:

The most important capital-structure development is the scale of STRC. In the Q4 presentation, STRC was materially smaller; your latest image shows STRC at $8.537B notional, making it by far the largest preferred. That changes the analysis: STRC is no longer merely one preferred product among several. It is now the center of the preferred capital structure.

Strategy’s preferreds are supported by assets, not operating cash flow

Traditional preferred analysis starts with operating earnings and free cash flow. Strategy is different. The preferred stack is effectively supported by:

- Bitcoin asset value

- USD reserve liquidity

- Capital-market access

- Management willingness to defend preferred dividends

- Common equity market value as a residual shock absorber

Strategy’s business model is dominated by BTC treasury operations, not conventional enterprise cash generation. It reports $58.9B of digital assets at year-end 2025, $2.3B of cash and cash equivalents, $8.2B of long-term debt, $6.9B of preferred equity, and $44.2B of common equity as of the balance sheet update in that deck.

That earlier balance sheet has since been overtaken by the latest uploaded capital-stack image, particularly because preferred notional has expanded to $13.540B. The result is a much larger fixed or quasi-fixed dividend layer sitting between debt and common.

Product-by-product institutional analysis

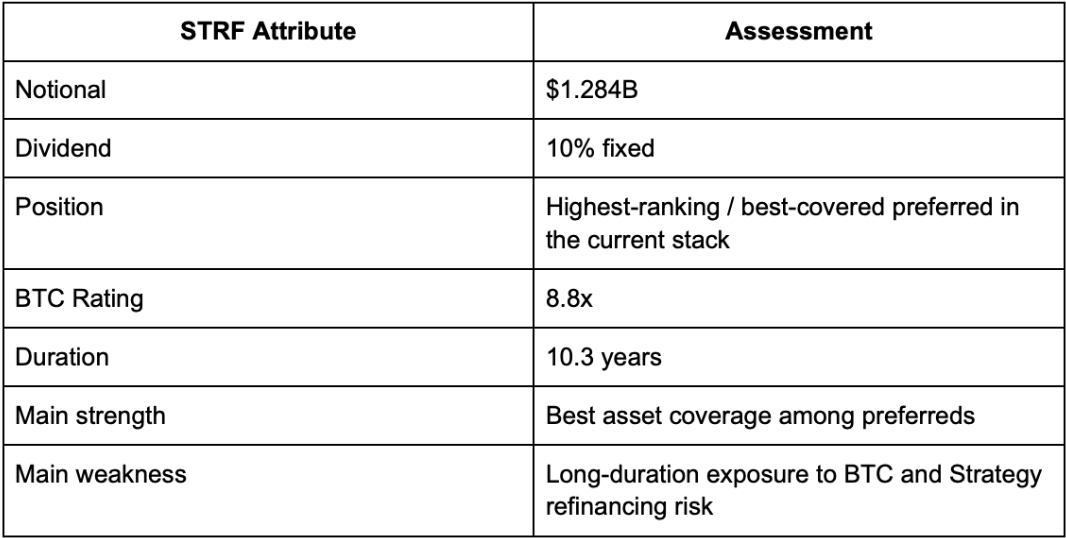

STRF: the cleanest preferred-credit instrument

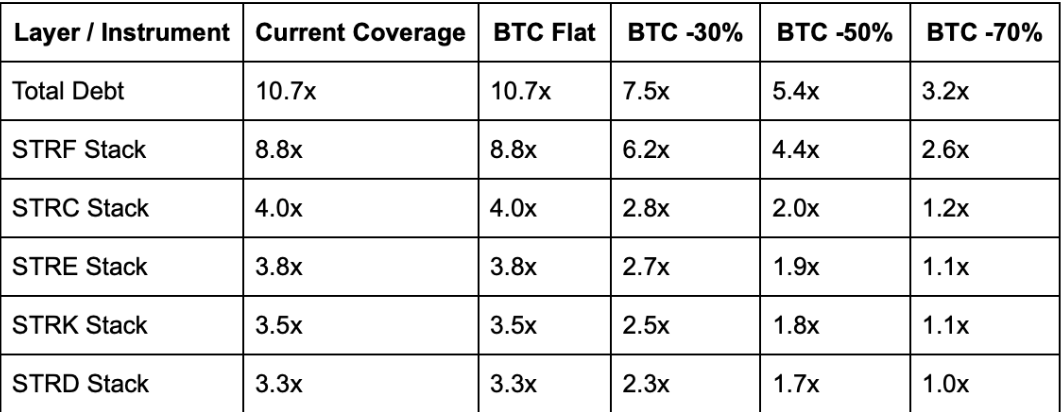

STRF is the strongest preferred from a pure credit perspective. In the latest stack, it has $1.284B notional, sits immediately after debt, has 8.8x BTC coverage, and has a 10.3-year duration.

STRF is best understood as the preferred suite’s senior credit proxy. It has no MSTR equity conversion upside like STRK and no variable-rate monthly design like STRC, but that simplicity is a strength. In a stress scenario, STRF’s higher position in the stack and smaller issue size make it the preferred most likely to retain institutional support.

The Q4 preferred overview labels STRF as “Lowest Risk,” which is consistent with its higher BTC coverage and fixed 10% dividend profile.

Institutional view: STRF is the best risk-adjusted preferred for conservative investors who still want exposure to Strategy’s BTC-linked credit.

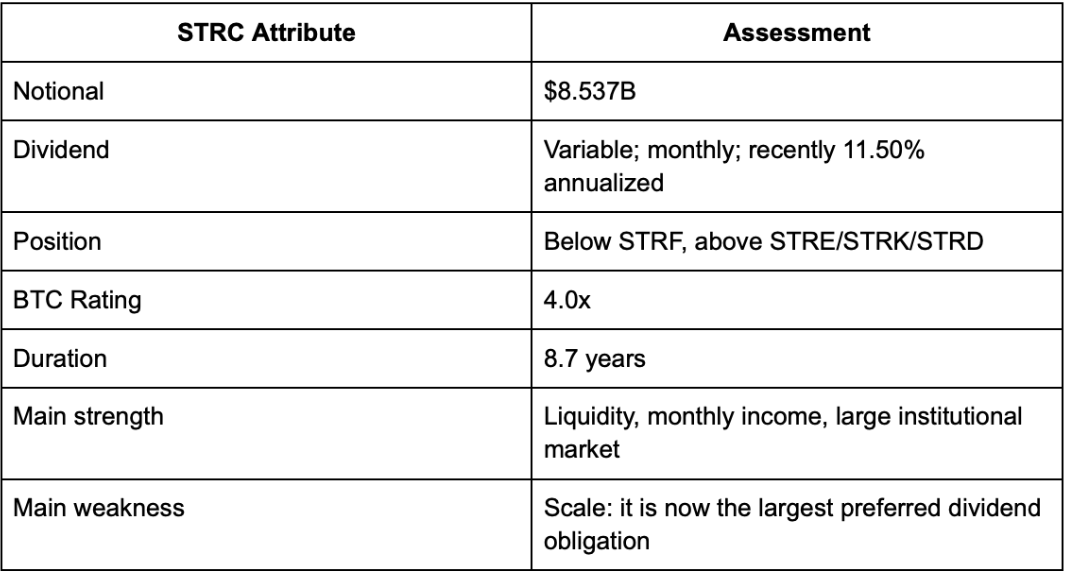

STRC: the dominant liquidity and income instrument

STRC is the most important preferred in the complex because of its size. The latest uploaded image shows $8.537B notional, far larger than any other preferred. It has 4.0x BTC coverage and 8.7-year duration.

The Q4 deck positions STRC as “Treasury Credit” and shows it as the most liquid preferred product. The deck reported $118M of 30-day average trading volume for STRC, materially higher than the other preferreds.

A later March 2026 filing showed Strategy declaring a monthly STRC dividend of $0.958333333 per share, equivalent to an 11.50% annualized dividend rate.

That high monthly income is attractive, but STRC’s size changes the risk profile. At $8.537B notional, every 1% of annual dividend rate represents roughly $85M of annual cash burden. At 11.50%, STRC alone requires roughly $982M per year. That is more than all other preferred dividends combined.

Institutional view: STRC is the preferred complex’s liquidity anchor. It may be the best trading instrument and income vehicle, but it is no longer the safest credit instrument because its scale creates meaningful dividend-burden risk.

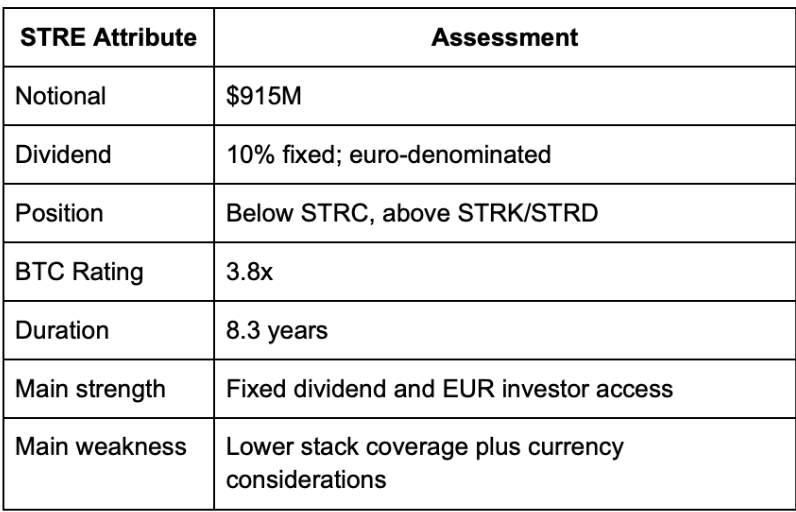

STRE: euro-denominated fixed preferred

STRE is the euro-denominated preferred. It has $915M notional, 3.8x BTC coverage, and 8.3-year duration in the latest image.

STRE is not the cleanest preferred for USD investors because the euro denomination introduces foreign-exchange considerations. But for European or euro-liability investors, it may be the preferred product that best matches currency needs.

Its smaller size is a credit positive, but its lower placement in the stack versus STRF and STRC is a negative. It has less BTC coverage than STRF and only slightly less than STRC, but without STRC’s trading liquidity.

A March 2026 filing showed a declared STRE dividend of €2.50 per share.

Institutional view: STRE is a specialized euro-denominated fixed-income product. It is not the strongest preferred, but it is relevant for investors seeking EUR income from Strategy’s BTC-linked capital structure.

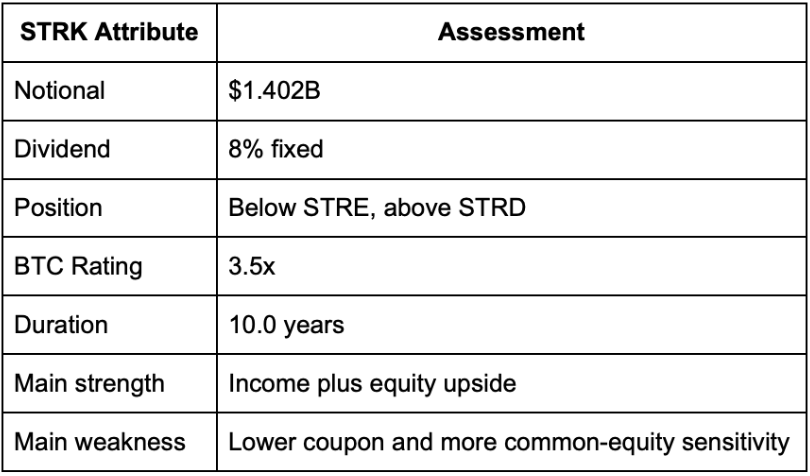

STRK: income plus MSTR upside

STRK is the preferred that most clearly bridges credit and equity. The Q4 deck describes STRK as the “Upside Exposure” product and indicates a 10:1 MSTR conversion feature.

STRK has a lower dividend rate than STRF, STRE, and STRD, but investors receive conversion optionality. That makes STRK better suited for investors who believe MSTR common will appreciate materially in a BTC bull market.

From a pure credit perspective, STRK is weaker than STRF and STRC: it has lower BTC coverage, a lower dividend, and greater sensitivity to common equity valuation. But that is the design. STRK is not meant to be the safest income product; it is a preferred instrument with embedded upside.

A March 2026 filing showed Strategy declaring a $2.00 per share STRK dividend.

Institutional view: STRK is most attractive for BTC bulls who want income while retaining some participation in MSTR equity upside. It is not the first choice for conservative income.

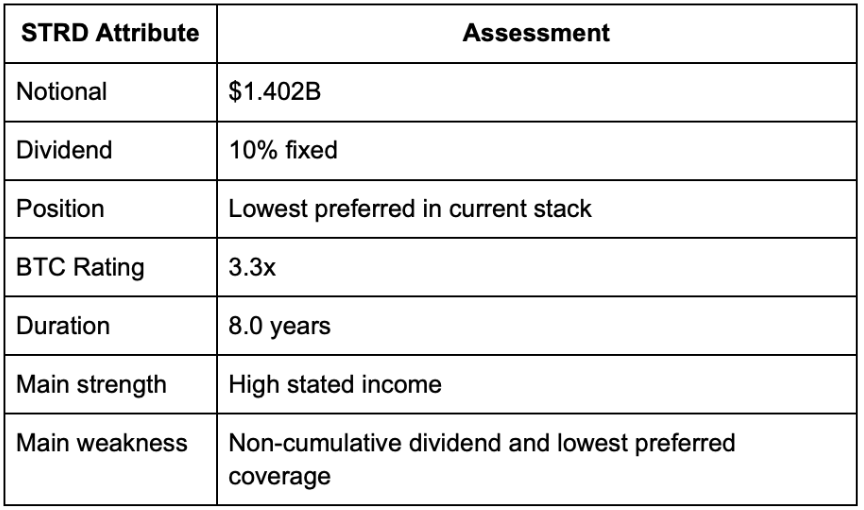

STRD: highest yield, weakest structure

STRD is the riskiest preferred in the suite. It has $1.402B notional, 3.3x BTC coverage, and 8.0-year duration in the latest image. The key issue is that it is non-cumulative.

The difference between cumulative and non-cumulative preferreds is central. If a cumulative preferred misses dividends, those unpaid dividends generally build as arrears. If a non-cumulative preferred misses a dividend, the investor has a weaker claim to recover that missed income. The prospectus language distinguishes cumulative and non-cumulative preferred mechanics, including different treatment of unpaid dividends for redemption or acquisition restrictions.

The Q4 preferred overview labels STRD as “Highest Yield,” which is correct economically, but the extra yield compensates for weaker structure.

A March 2026 filing showed Strategy declaring a $2.50 per share STRD dividend, but the existence of a declared dividend does not eliminate the structural risk of non-cumulative treatment in future stress.

Institutional view: STRD is suitable only for investors who are deliberately accepting higher dividend-suspension risk in exchange for higher yield. It is the weakest preferred for conservative credit investors.

Dividend coverage and liquidity runway

Using the latest image and recent dividend rates, the estimated annual cash burden is:

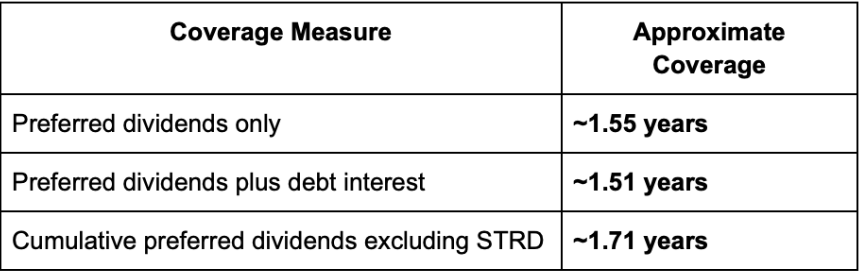

With a $2.250B USD reserve, the reserve covers approximately:

This is an important shift from the Q4 2025 deck, which showed $888M of annual cash burden and described the USD reserve as providing about 2.5 years of dividend coverage. The difference is driven mainly by the larger STRC notional in the latest image.

The implication is clear: the USD reserve is still meaningful, but under the latest stack it is no longer a multi-year fortress. The dividend model increasingly depends on Strategy maintaining capital-market access, BTC asset coverage, and investor confidence.

BTC downside stress test

The preferreds are highly sensitive to BTC because Strategy’s asset base is dominated by Bitcoin. Strategy’s BTC holdings at 815,061 BTC, equal to 3.4% of all BTC ever to be in existence.

Using the latest image’s BTC rating/coverage figures and applying simple linear BTC price shocks:

BTC flat

In a flat BTC environment, the preferreds are primarily a liquidity and dividend-coverage story. Debt remains well-covered, and all preferreds retain meaningful asset coverage. STRF looks best from a credit perspective; STRC likely trades best because of liquidity and monthly income.

BTC down 30%

At a 30% BTC decline, debt remains comfortably covered, but lower-stack preferreds begin to trade with more equity sensitivity. STRF would likely outperform because its coverage remains above 6x. STRD would likely underperform because it is both lowest in the stack and non-cumulative.

BTC down 50%

A 50% BTC decline would probably reprice the entire preferred complex. Debt still appears covered in a simplified asset-coverage framework, but preferred coverage compresses meaningfully. STRC falls to around 2.0x coverage, and STRD to around 1.7x. The market would likely focus on dividend sustainability, capital-market access, and whether Strategy can avoid issuing securities at distressed prices.

BTC down 70%

At a 70% BTC decline, the preferreds become deeply stressed. Total debt still has theoretical coverage, but the full debt-plus-preferred stack approaches roughly 1.0x coverage. In this scenario, preferred prices could behave like distressed equity-linked securities. STRF remains the best protected; STRD is the most exposed.

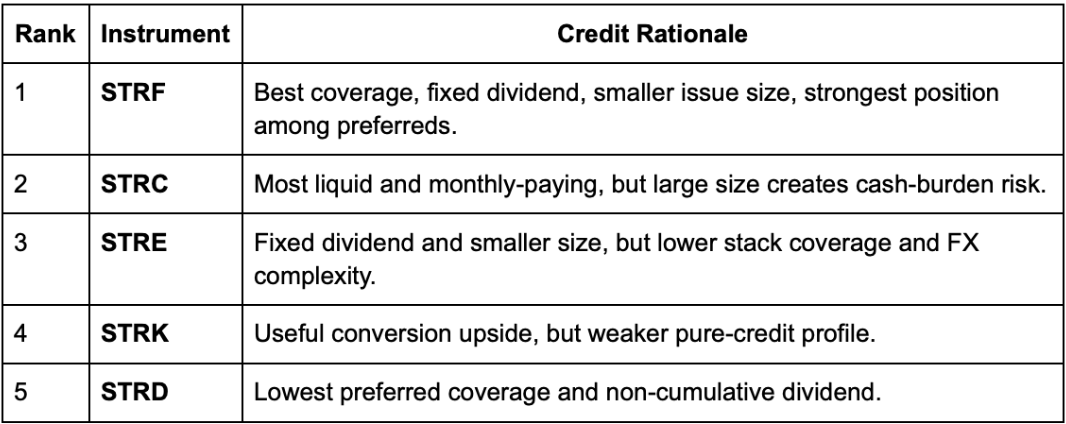

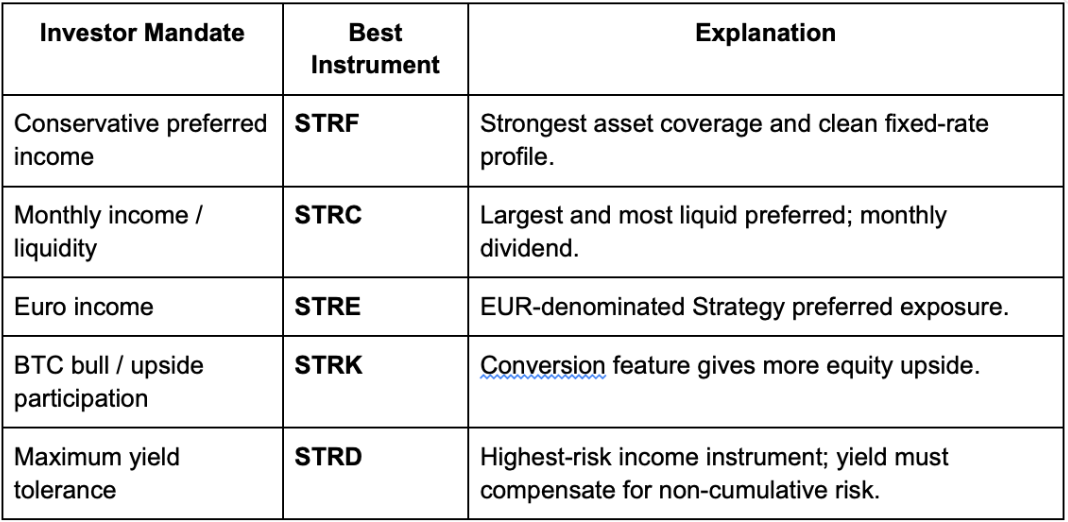

Relative value ranking

Credit ranking

Relative value by mandate

Key risks

BTC price risk

This is the dominant risk. The preferreds are ultimately claims on a company whose enterprise value is driven by Bitcoin. BTC declines reduce asset coverage, common equity cushion, refinancing options, and investor confidence.

Dividend discretion risk

Preferred dividends are not debt interest. The prospectus states that dividends are payable only when declared by the board.

Cumulative vs non-cumulative risk

STRD’s non-cumulative structure makes it materially weaker than the other preferreds. In a stress scenario, missed dividends do not provide the same arrears protection as cumulative preferreds.

Issuance risk

The base prospectus and ATM program contemplate ongoing issuance of common and preferred stock. Issuance can be positive if proceeds buy BTC accretively, but negative if it increases dividend burden faster than asset coverage. The prospectus describes sales of class A common stock and preferred stock from time to time through agents under an at-the-market style program.

Liquidity risk

STRC appears to have the best trading liquidity. Other preferreds may be more vulnerable to sharp price gaps in stress, especially STRD and STRE.

Common equity dependency

Common equity is the residual shock absorber. If MSTR common trades well, Strategy’s capital-market access improves. If common equity weakens materially, refinancing and preferred issuance become more expensive, putting more pressure on the preferred complex.

Conclusion

Strategy’s preferred suite is best understood as a laddered set of BTC-linked capital instruments, not a homogeneous preferred-stock class.

STRF is the institutional credit choice. It has the strongest coverage and the cleanest fixed-income profile.

STRC is the institutional liquidity choice. It is the product most likely to attract income funds and trading desks, but its sheer size means it now drives the cash burden of the entire preferred stack.

STRE is a euro-denominated niche product. It may be compelling for EUR-based investors, but it is not the best USD credit instrument.

STRK is the preferred for BTC bulls who want income with embedded MSTR upside.

STRD is the speculative yield product. Its non-cumulative structure and lowest coverage make it the weakest preferred from a downside-protection perspective.

The preferred complex remains investable only under a clear assumption: Strategy must maintain sufficient BTC asset coverage, USD liquidity, and capital-market access to keep supporting a large and growing preferred dividend stack. Among the instruments, STRF offers the best downside-adjusted profile, STRC offers the best liquidity and income mechanics, and STRD requires the highest risk premium.

FOLLOW US ON:

X (Twitter), Youtube, Instagram, Linkedin

Access to these products and services is restricted to non-U.S. persons and may not be available in certain jurisdictions.