SWC’s Smart Warrant Cleanup: How 39 Million Cancelled Warrants Strengthened the Bitcoin-per-Share Story

The Smarter Web Company used modest short-term debt to remove a major dilution overhang, simplify its capital structure, and increase Satoshis per share from 680 to 755.

The Setup: A Company Cleaning Up Its Capital Structure

The Smarter Web Company PLC has been building a very specific public-market identity a UK-listed company with a Bitcoin treasury strategy.

For shareholders, this means the story is not only about ordinary business growth. It is also about one very important question:

How much Bitcoin exposure does each share represent?

That is why the company’s recent warrant transaction matters.

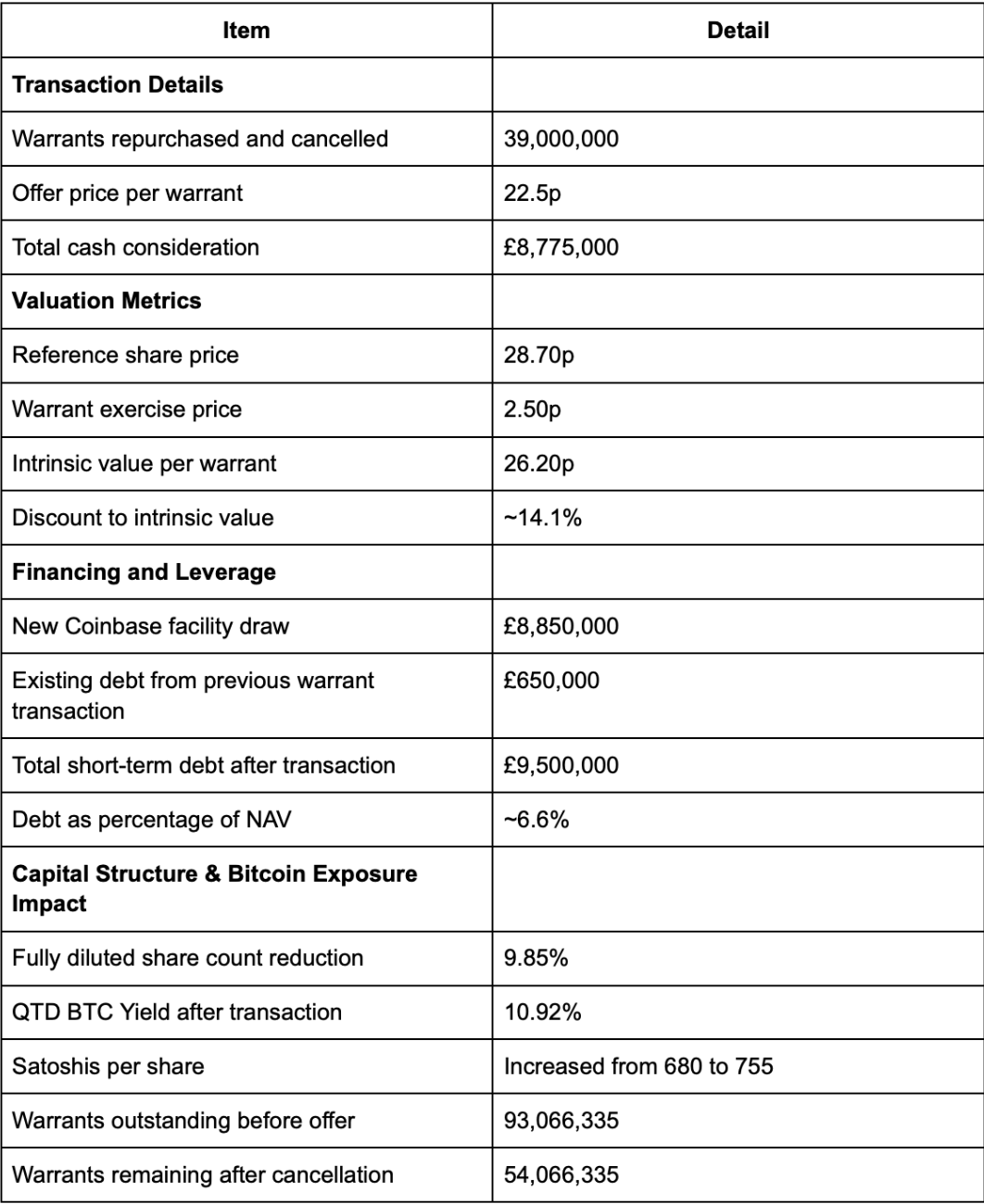

SWC bought and cancelled 39,000,000 Pre-IPO Warrants at 22.5p per warrant. The total cash cost was £8,775,000. The company funded the purchase by drawing £8,850,000 from its Coinbase Strategic Credit Facility, which brought total short-term debt to £9,500,000, equal to approximately 6.6% of NAV.

In simple words: SWC borrowed money to remove a large block of future dilution.

That is the heart of the story.

What Is a Warrant, in Plain English?

A warrant is like a special ticket that lets someone buy shares in the future at a fixed price.

In SWC’s case, these Pre-IPO Warrants allowed holders to buy shares at only 2.5p per share. They were exercisable between 24 April 2026 and 24 April 2028.

Now imagine the company’s shares are trading at 28.70p, but someone has a ticket that lets them buy at 2.5p.

That ticket is valuable because the holder can buy shares far below the market price.

The basic value of that warrant is:

28.70p reference share price − 2.50p exercise price = 26.20p intrinsic value

SWC offered to buy those warrants for 22.5p each, which was approximately a 14.1% discount to intrinsic value.

So SWC did not pay full value. It bought back the warrants at a discount.

The Problem: Cheap Future Shares Hanging Over the Market

Before the offer, there were 93,066,335 Pre-IPO Warrants outstanding.

That is a big number.

If those warrants were exercised, SWC would have to issue many new shares at just 2.5p. For existing shareholders, that creates dilution.

Dilution is like owning a slice of pizza. If the company creates more slices, your slice becomes a smaller percentage of the whole pizza.

For a Bitcoin treasury company, this matters even more.

Why?

Because shareholders are watching Bitcoin per share. If more shares are created, the company’s Bitcoin exposure gets spread across more shares. That can reduce each shareholder’s effective Bitcoin exposure.

So these warrants were not just a technical detail. They were a visible overhang.

Investors could look at the company and think:

“Before I buy this stock, what happens when all these cheap warrants become exercisable?”

SWC’s transaction directly addressed that concern.

The Smart Move: Paying Cash Today to Avoid Dilution Tomorrow

SWC chose to pay cash now to remove future dilution.

The company purchased 39,000,000 warrants from 210k Capital L.P., a related party affiliated with Non-Executive Director Tyler Evans. Those warrants were then cancelled.

This means those 39,000,000 potential future shares disappeared from the fully diluted share count.

That is why the transaction is important.

SWC did not simply spend money. It used capital to clean up its share structure.

In everyday language, this is like a homeowner paying off a future claim on their house before it becomes a problem. The house does not become bigger overnight, but the ownership becomes cleaner.

For ordinary shareholders, the result was meaningful: the transaction reduced the fully diluted share count by 9.85% and increased Quarter-to-Date BTC Yield to 10.92%.

The Numbers That Matter

Here are the key numbers in one place:

The simplest summary is this:

SWC paid £8.775 million to cancel 39 million future low-cost shares.

That helped existing shareholders because fewer future shares means each remaining share can represent more of the company’s Bitcoin treasury.

Why This Looks Good for Ordinary Shareholders

This transaction looks shareholder-friendly for several reasons.

First, SWC bought the warrants at a discount. The intrinsic value was 26.20p, but the company paid 22.5p. That is approximately a 14.1% discount.

Second, the company removed 39,000,000 future shares of dilution.

Third, the fully diluted share count fell by 9.85%.

Fourth, the company’s Quarter-to-Date BTC Yield increased to 10.92%.

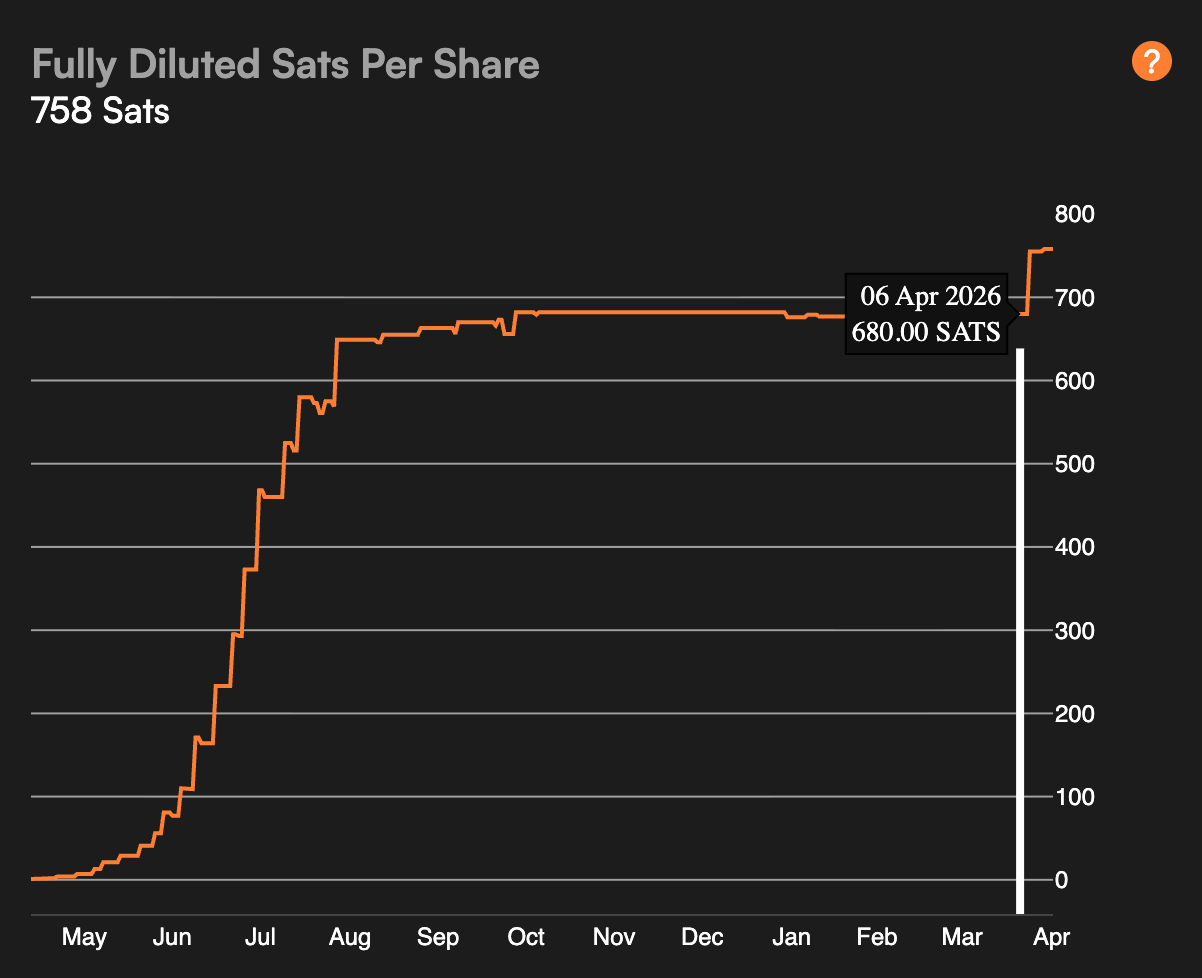

Fifth, management explained that Satoshis per share increased from 680 to 755.

That is the key point for a Bitcoin treasury company.

SWC did not need to buy more Bitcoin to increase Satoshis per share. It increased the Bitcoin exposure per share by reducing the number of future shares.

For shareholders who care about long-term Bitcoin-per-share growth, that is a strong result.

The Bitcoin Treasury Angle: More Satoshis Per Share

In a normal company, investors often focus on earnings per share.

In a Bitcoin treasury company, investors also focus on Satoshis per share.

A Satoshi is the smallest unit of Bitcoin.

So when management says Satoshis per share increased from 680 to 755, it means each fully diluted share now represents more Bitcoin exposure than before.

This is why the transaction matters so much.

The company reduced the number of future shares that could claim ownership of the same Bitcoin treasury.

That is like having the same amount of Bitcoin in the vault, but fewer claim tickets on that vault.

For ordinary shareholders, that can be powerful.

Why Reducing the Overhang Matters

A warrant overhang can quietly hurt a stock.

Even if the warrants have not been exercised yet, investors know they are there. They may worry that once the warrants become exercisable, holders could buy shares cheaply and sell them into the market.

That fear can weigh on sentiment.

By cancelling 39,000,000 warrants, SWC removed a major part of that concern.

Before the offer, there were 93,066,335 Pre-IPO Warrants outstanding. After the cancellation, 54,066,335 Pre-IPO Warrants remained outstanding.

So the overhang was not eliminated completely.

But it was reduced meaningfully.

For institutions and long-term investors, that cleaner structure can make the equity story easier to understand.

And in public markets, simplicity matters.

The Debt Caveat: The Deal Was Not Free

This is the main caveat.

SWC funded the transaction with debt.

The company drew £8,850,000 from its Coinbase Strategic Credit Facility. Including £650,000 of existing debt from a previous warrant transaction, total short-term debt rose to £9,500,000.

That represented approximately 6.6% of NAV.

This is not a huge leverage number, but it is still leverage.

Debt can be useful if it helps create shareholder value. But debt also needs to be repaid.

The company said it intends to repay the debt through a combination of operational cash flow and future equity issuance.

That is where investors should pay attention.

If future equity is issued on attractive terms, the transaction remains very strong. But if equity is issued at unattractive levels, some of the benefit from cancelling the warrants could be diluted away.

So the deal is bullish, but not risk-free.

The Governance Question: Understanding the Related-Party Angle

There is also a governance angle.

The seller of the 39,000,000 warrants was 210k Capital L.P., which is affiliated with Non-Executive Director Tyler Evans. That makes it a related-party transaction.

In simple language, a related-party transaction means the company is doing business with someone connected to the company.

That does not automatically mean something is wrong. But it does mean shareholders should look carefully at whether the terms are fair.

There are several important mitigants here.

The offer was available to all warrant holders. The price was set at a discount to intrinsic value. The Board said the terms were fair and reasonable and had been advised by the company’s sponsor, Strand Hanson. Also, Andrew Webley, his spouse, and other directors/employees did not participate in the offer.

That last point matters.

Management did not use the offer to cash out its own warrants. Instead, the CEO and spouse continued to hold 25,778,732 warrants, while directors/employees held a further 1,450,000 warrants.

So while the related-party angle deserves attention, the structure appears designed to reduce governance concerns.

What Could Still Go Wrong?

The bullish case is strong, but investors should still understand the risks.

First, the transaction was funded with debt. Debt increases financial pressure and needs to be repaid.

Second, future equity issuance may be needed. If new shares are issued at unattractive levels, some of the benefit from this warrant cancellation could be reduced.

Third, the company remains exposed to Bitcoin volatility. If Bitcoin falls sharply, NAV can fall too.

Fourth, the related-party optics may concern some shareholders, even though the offer was available to all warrant holders and management did not tender.

Fifth, 54,066,335 Pre-IPO Warrants still remain outstanding, so the warrant overhang is reduced but not completely gone.

Finally, BTC Yield is useful, but it is not the same as profit, cash flow, or total shareholder return. It is a Bitcoin-per-share metric, not a guarantee that the share price will rise.

Final Takeaway: A Bullish Capital-Structure Move

The Smarter Web Company’s warrant repurchase looks like a smart, shareholder-friendly capital-structure move.

The company used modest leverage to cancel 39,000,000 future shares of potential dilution. It bought the warrants at a discount to intrinsic value. It reduced the fully diluted share count by 9.85%. It increased Quarter-to-Date BTC Yield to 10.92%. And management said Satoshis per share increased from 680 to 755.

For a Bitcoin treasury company, those are important outcomes.

The transaction makes the capital structure cleaner, reduces a major overhang, and improves fully diluted Bitcoin economics for ordinary shareholders.

The main caveat is that the company used debt to do it. So the next important question is how SWC repays that debt and whether any future equity issuance is done on attractive terms.

But on the numbers disclosed, the deal looks strategically sensible.

SWC exchanged modest short-term leverage for a cleaner structure, lower dilution, and stronger Bitcoin-per-share metrics. For ordinary shareholders, that is a bullish outcome provided the company continues to manage the balance sheet carefully.

FOLLOW US ON:

X (Twitter), Youtube, Instagram, Linkedin

Access to these products and services is restricted to non-U.S. persons and may not be available in certain jurisdictions.