STRC vs SATA: How the Market Is Pricing Bitcoin Credit Risk

Why two Bitcoin-linked preferred securities with similar durations can trade at meaningfully different yields

When investors look at Bitcoin-linked income products, the first instinct is often to compare the coupon and stop there. One instrument yields more, another yields less, and the market appears to be giving a verdict. But that surface-level reading misses the real question.

The deeper issue is not simply which security pays the higher yield. It is why the market demands that yield in the first place.

That is what makes the comparison between STRC and SATA so interesting. Both are preferred instruments tied, directly or indirectly, to Bitcoin-heavy corporate balance sheets. Both sit within emerging capital structures that use Bitcoin as a treasury reserve asset. Both can be analyzed through the lens of Bitcoin coverage, expected duration, and balance-sheet support. And yet the market prices them differently. SATA carries a meaningfully higher effective yield than STRC, despite a capital structure that is in some respects simpler.

Understanding that gap requires more than a bullish or bearish view on Bitcoin. It requires a framework for thinking about Bitcoin credit risk, capital structure hierarchy, and the difference between what mathematics suggests and what markets actually reward.

At its core, this is not just a story about two securities. It is a story about how the market is beginning to price an entirely new category of financial product Bitcoin-powered credit.

A new way to think about Bitcoin-linked income

Traditional credit analysis starts with familiar questions. How much debt is outstanding? What assets support it? What sits above or below it in the capital structure? What is the probability of impairment over time?

Those questions still apply here, but with an important twist: Bitcoin itself becomes part of the credit analysis.

That is why newer analytical frameworks use terms like BTC Rating, BTC Risk, and BTC Credit to compare Bitcoin-backed instruments. BTC Rating measures the amount of notional debt outstanding relative to the Bitcoin held on the balance sheet, with a higher ratio indicating a larger Bitcoin buffer relative to that liability layer. BTC Risk estimates the probability that the Bitcoin coverage falls below 1x by the end of the instrument’s duration. BTC Credit then translates that long-term risk into an annualized credit spread, making it easier to compare with traditional fixed-income products.

For a layman, the easiest way to think about this is simple: if a company has a large Bitcoin treasury and relatively modest preferred obligations, that preferred layer may be better supported than its headline structure alone would suggest. The market, however, does not price support in a purely mechanical way. It also prices scale, reputation, liquidity, and corporate history.

STRC: the power of scale and institutional history

On paper, STRC benefits from the thing markets usually reward most: institutional familiarity.

Strategy, the issuer behind STRC, operates at a scale that dwarfs most other Bitcoin treasury companies. It has spent years in the capital markets, repeatedly raising funds, issuing securities, and educating investors around its Bitcoin-centric strategy. That track record matters. In financial markets, scale and repetition often reduce perceived risk even when balance sheets are complex.

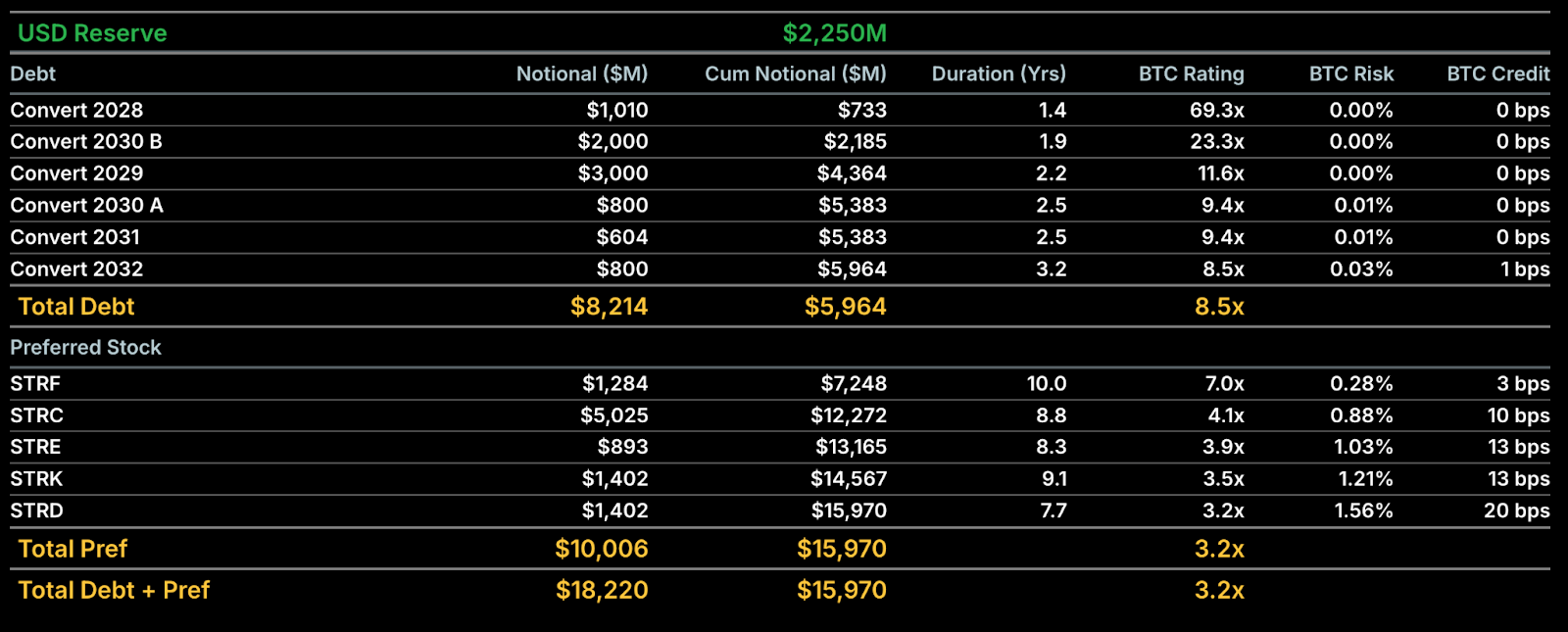

This matters because STRC does not sit inside a simple structure. Senior to preferred instruments like STRC is a substantial layer of convertible debt. According to the comparison framework in the provided text, Strategy carries over $8.2 billion in senior convertible notes, meaning STRC is structurally subordinate to a very large amount of senior capital.

That would normally be a major negative. And in a purely traditional capital-structure analysis, it is. But markets do not look only at the stack above the preferred. They also look at the issuer’s ability to keep raising capital, maintain investor confidence, and navigate periods of volatility. Strategy’s long history in public markets appears to buy it a meaningful premium in that regard.

In other words, STRC benefits not just from Bitcoin support, but from the market’s belief that the issuer itself is a seasoned operator in a still-young category.

SATA: simpler structure, smaller scale, higher yield

SATA sits in a very different position.

Strive and do not yet have the same capital-markets history, institutional scale, or market mythology as Strategy. That matters, because in credit markets investors do not merely underwrite balance sheets. They also underwrite management credibility, financing flexibility, and familiarity. Smaller issuers almost always pay more.

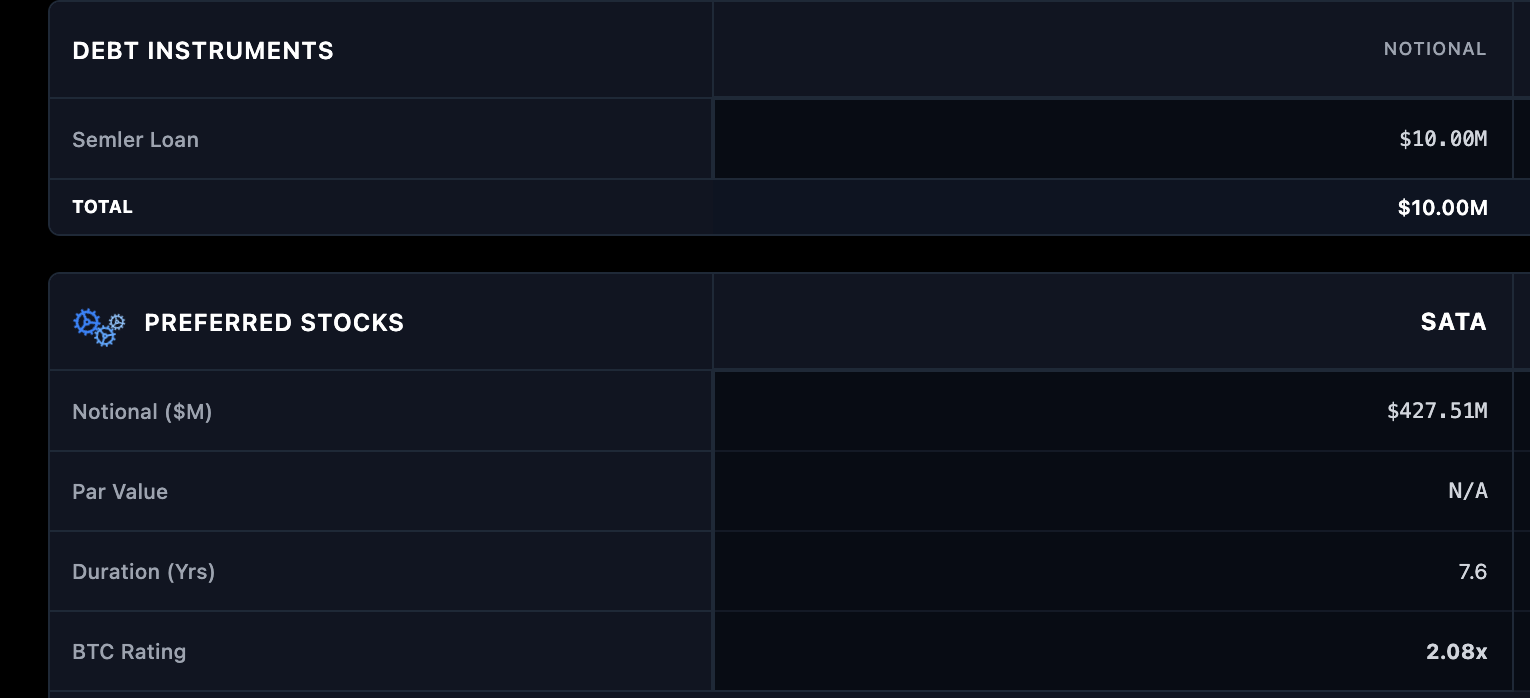

Yet SATA also has an advantage that deserves more attention: its capital structure is much simpler. According to the comparison in the uploaded text, sitting senior to SATA is only a $10 million standard loan. In other words, SATA effectively sits just behind a relatively modest senior claim in the repayment hierarchy.

That simplicity is not trivial. For many investors, a cleaner capital structure is easier to understand and easier to underwrite. It removes much of the uncertainty that comes from multi-billion-dollar layers of convertible debt sitting above the preferred. It also means the security’s relationship to the underlying reserve asset base can, in some respects, be more direct and easier to model.

And yet the market still demands more yield from SATA. That is the central puzzle.

The balance-sheet structures shows that SATA’s BTC Rating is about 2.1x, compared with STRC’s roughly 4.1x. That means SATA has a smaller Bitcoin cushion relative to its notional liability layer, even though its capital structure is cleaner. At the same time, SATA’s effective yield is roughly 12.8%, versus 11.5% for STRC(these no’s are according to 31st march), a difference of about 137 basis points.

That spread is where the real analytical work begins.

The mathematics say one thing the market says another

Using the following assumptions 30% long-term annual Bitcoin returns and 45% volatility the model estimates STRC’s credit spread at about 9.4 to 10 basis points and SATA’s at approximately 44.8 to 45 basis points. That implies a mathematically derived difference in credit risk of about 35 basis points.

But the market spread between the two instruments is much larger: about 137 basis points. That means the actual pricing gap exceeds the modeled credit-risk gap by around 102 basis points.

That divergence is one of the most important insights in the comparison.

It suggests that markets are not pricing STRC and SATA based solely on Bitcoin coverage math. They are applying a substantial premium to scale, issuer history, and institutional familiarity. They are also likely building in more conservative assumptions around Bitcoin’s long-term path than the base model assumes. According to the text, for the 137-basis-point market spread to align perfectly with the model, one would need to assume something closer to 21% annual Bitcoin returns and 50% volatility.

That is a subtle but critical conclusion. It implies that the market may be pricing SATA not merely as a riskier preferred, but as a preferred attached to a younger, less established Bitcoin capital-markets platform.

Why capital structure still matters

The easiest mistake investors can make in this comparison is to reduce everything to the BTC Rating.

A higher BTC Rating does matter. A larger Bitcoin cushion relative to the notional liability is a real credit positive. On that basis, STRC deserves some premium over SATA. But that is not the whole story.

Capital structure matters too. And here SATA has a credible counterargument. While SATA’s BTC Rating is lower, it is supporting a structure with comparatively little senior debt. STRC, by contrast, sits beneath a very large layer of senior convertible obligations. Investors therefore face a real trade-off: do they prefer the larger Bitcoin cushion of STRC, or the simpler and cleaner repayment hierarchy of SATA?

This is where the comparison becomes more nuanced than a simple “higher rating is better” framework.

In a liquidation or restructuring context, the amount and complexity of senior claims matter enormously. A preferred stock with a lower BTC Rating but fewer claims ahead of it may, in some scenarios, look more attractive than a preferred stock with a stronger Bitcoin cushion but a much heavier senior stack. That does not automatically make SATA safer. It does mean the structure deserves more credit than a superficial comparison might suggest.

For professional investors, this is the key point: SATA is not simply “weaker STRC.” It is a different kind of credit proposition.

The duration profile makes the comparison even tighter

Another reason the STRC-SATA comparison matters is that their expected holding periods are relatively close.

The uploaded analysis places STRC at an approximate duration of 8.7 years and SATA at about 7.6 to 7.7 years. That similarity is important because it removes one common excuse for major yield differences. If one instrument had dramatically longer duration, a large yield spread would be easier to justify. But when the durations are broadly comparable, the pricing difference starts to look more like a statement about issuer perception and structural confidence than about simple time exposure.

That is another reason the 137-basis-point gap stands out. The instruments are close enough in duration that the market is clearly charging SATA a meaningful premium for something other than just tenor.

And that “something” appears to be a mix of smaller scale, shorter history, and the uncertainty premium that younger Bitcoin credit products still carry.

Final conclusion

Comparing STRC and SATA requires more than reading the coupon and picking the higher number. It requires balancing quantitative Bitcoin-coverage analysis with qualitative judgments about scale, issuer history, and capital-structure design.

STRC benefits from a larger Bitcoin cushion and the institutional premium that comes with Strategy’s history and size. SATA, by contrast, comes with a lower BTC Rating and a higher required yield, but also with a far simpler capital structure and relatively little senior debt standing ahead of it. The result is a market spread that is substantially wider than the mathematical risk gap alone would suggest.

That divergence is the heart of the opportunity.

For investors who believe markets sometimes overpay for familiarity and underpay for structural simplicity, SATA deserves close attention. It may not yet command the same premium as STRC, but that is precisely why it may offer more compelling value. In a market still learning how to price Bitcoin-powered credit, the most interesting opportunities often appear where the math and the market have not fully converged.

FOLLOW US ON:

X (Twitter), Youtube, Instagram, Linkedin

Access to these products and services is restricted to non-U.S. persons and may not be available in certain jurisdictions.