SATA: Engineering Near-Par Stability in a Bitcoin-Linked Preferred

Why Strive’s preferred stock may be evolving into one of the most compelling income instruments in digital finance

In traditional markets, income investors are usually forced to compromise. They can hold cash and earn modest yields with high stability, or they can reach for yield in preferred stock, private credit, or high-yield debt and accept more complexity, more volatility, or more credit risk. What they rarely get is a product explicitly designed to deliver double-digit monthly income, maintain near-par price behavior, and sit atop a balance sheet shaped by one of the most powerful reserve assets of the last decade.

That is the ambition behind SATA, Strive’s Variable Rate Series A Perpetual Preferred Stock.

At first glance, SATA looks like an unusual preferred stock. At second glance, it looks more like a new category: a managed income instrument engineered for the Bitcoin era. It has a $100 stated amount, pays a monthly dividend if declared by the board, and carries cumulative unpaid dividends, meaning missed dividends do not disappear. By March 2026, Strive had raised SATA’s variable annualized dividend rate to 12.75%, tightened its targeted trading range to $99 to $101, added a $50 million STRC position to support reserves, and stated that cash, STRC, and Bitcoin together covered more than 19 years of SATA dividend obligations under then-current assumptions.

That does not make SATA risk-free. It does make it important.

Because what Strive appears to be building is not just another preferred stock. It is trying to create a Bitcoin-supported credit product that offers income investors something they usually do not get from Bitcoin-related strategies: cash yield, range discipline, and a deliberately managed liability structure.

What SATA actually is ?

The easiest way to understand SATA is to strip away the jargon.

SATA is a preferred stock, which means it sits above common stock in the capital structure. In simple terms, preferred holders generally have a stronger economic claim than ordinary shareholders, but weaker protection than secured lenders. SATA is also perpetual, meaning it has no maturity date like a bond. And it is variable rate, meaning the dividend can be adjusted over time within the rules of the instrument rather than remaining permanently fixed.

The core terms matter. SATA has a $100 stated amount. Its regular dividends are paid monthly, in arrears, and by March 2026 the annualized rate had been set at 12.75%. If dividends are not paid, they are cumulative, and unpaid amounts can compound upward over time, which gives the instrument more teeth than a simple discretionary payout.

That balance is critical. SATA is not a bond. It is not a money market fund. And it is not a direct Bitcoin claim. It is a preferred equity instrument that attempts to behave more predictably than common stock while offering materially higher income than most conventional short-duration products. The March deck explicitly says SATA is not collateralized by Bitcoin and that owning SATA does not mean owning the Bitcoin itself. Instead, SATA has a preferred claim on the residual assets of the company, which means Bitcoin matters as balance-sheet support, not as pledged collateral.

For a layman, that means SATA is best understood as a high-income claim on Strive’s financial structure, not a tokenized Bitcoin bond and not a simple deposit substitute.

SATA different from a normal preferred stock

Many preferred stocks are static. They are issued, they pay a coupon, and then the market decides where they trade. SATA is different because Strive has been unusually explicit that it intends to manage the instrument’s behavior.

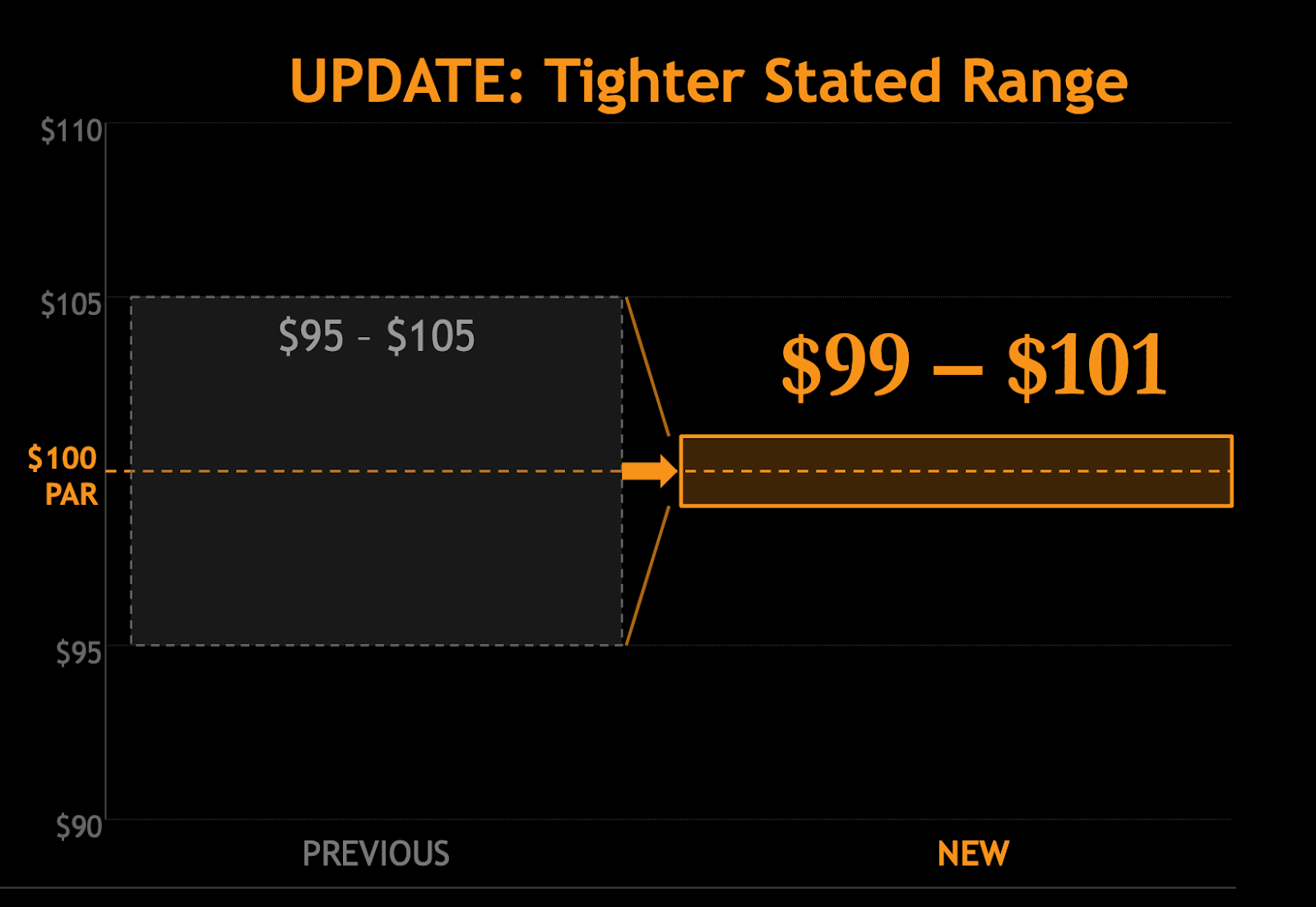

In January 2026, the company described SATA with a targeted trading range of $95 to $105. By March 2026, that range had narrowed to $99 to $101. At the same time, the company updated guidance to say it does not plan to issue new SATA below $100. The combination matters because it shows Strive is not merely selling yield. It is trying to create a preferred that trades near par and feels more stable than the average perpetual security.

That may sound cosmetic, but it is not. For income products, price behavior is part of the product itself. A preferred that yields 12.75% but regularly drifts to the low 90s feels very different from one that remains tightly anchored near $100. By tightening its stated range and signaling discipline on new issuance, Strive is effectively telling the market that SATA is meant to function as a managed near-par income security, not just a high-coupon perpetual floating in the market.

This is one of the most bullish features of the structure. It suggests the company understands that institutional credibility in income products comes not only from headline yield, but also from price discipline, reserve visibility, and issuance credibility.

The January blemish that made the March story stronger

No serious assessment of SATA can ignore the biggest awkward fact in its recent history: in January 2026, Strive priced a follow-on SATA offering at $90 per share, while also exchanging approximately 930,000 SATA shares for $90 million of Semler convertible notes. The transaction was large, the demand was significant, and the company said it had more than $600 million of demand, but the issuance below par clearly mattered.

Why did it matter? Because SATA’s entire promise rests partly on the idea that this is a managed credit-like instrument meant to live around par. Issuing a large block at $90 sends the opposite signal. It tells investors that when strategic priorities are pressing, management may prioritize financing flexibility over par protection.

Yet this is precisely why the March changes are important. By March, the company had responded with a tighter $99 to $101 target range and explicit guidance that it does not plan to issue new SATA below $100.

The bullish interpretation is not that January did not matter. It is that January looks increasingly like a transitional financing event, while March looks like a maturing product policy. In other words, the structure appears to be learning in public, and learning in the right direction.

For institutional investors, that is often good enough. The question is rarely whether a structure began perfectly. The question is whether it is becoming more disciplined, more defensible, and more aligned with the market it wants to serve. On that score, SATA appears to be improving.

The capital-structure cleanup was the real turning point

The single most important thing Strive did for SATA may not have been increasing the dividend. It may have been cleaning up the balance sheet around it.

By January 28, 2026, Strive said it had retired $90 million of Semler convertible notes in exchange for SATA shares and used part of the cash proceeds from the offering to retire the $20 million Coinbase loan. The company further stated that, after repaying the Coinbase loan, 100% of its Bitcoin holdings were unencumbered, and that roughly 92% of the inherited debt had been retired within days of the Semler acquisition, with an intention to retire the rest by April 2026.

This matters because preferred stock does not exist in a vacuum. The real safety of a preferred instrument depends heavily on what sits ahead of it. If a company carries a large amount of debt, secured claims, or encumbrances on core assets, preferred holders are naturally weaker. When those debts are retired and the core reserve asset becomes unencumbered, the effective position of the preferred improves even if its legal ranking does not change.

That is what happened here. SATA still is not secured by Bitcoin. But a preferred claim backed by a cleaner capital structure and a large unencumbered Bitcoin treasury is materially more compelling than a preferred claim buried under legacy obligations.

This is one reason the SATA thesis has become much easier to defend. The instrument itself is unusual, but the corporate architecture supporting it is getting cleaner, simpler, and more intentional.

The dividend is high, but the reserve story is what makes it interesting

A 12.75% annualized dividend will always attract attention. But plenty of high-yield instruments look good at the top line and fragile underneath. What gives SATA more substance is the reserve framework Strive has built around that payout.

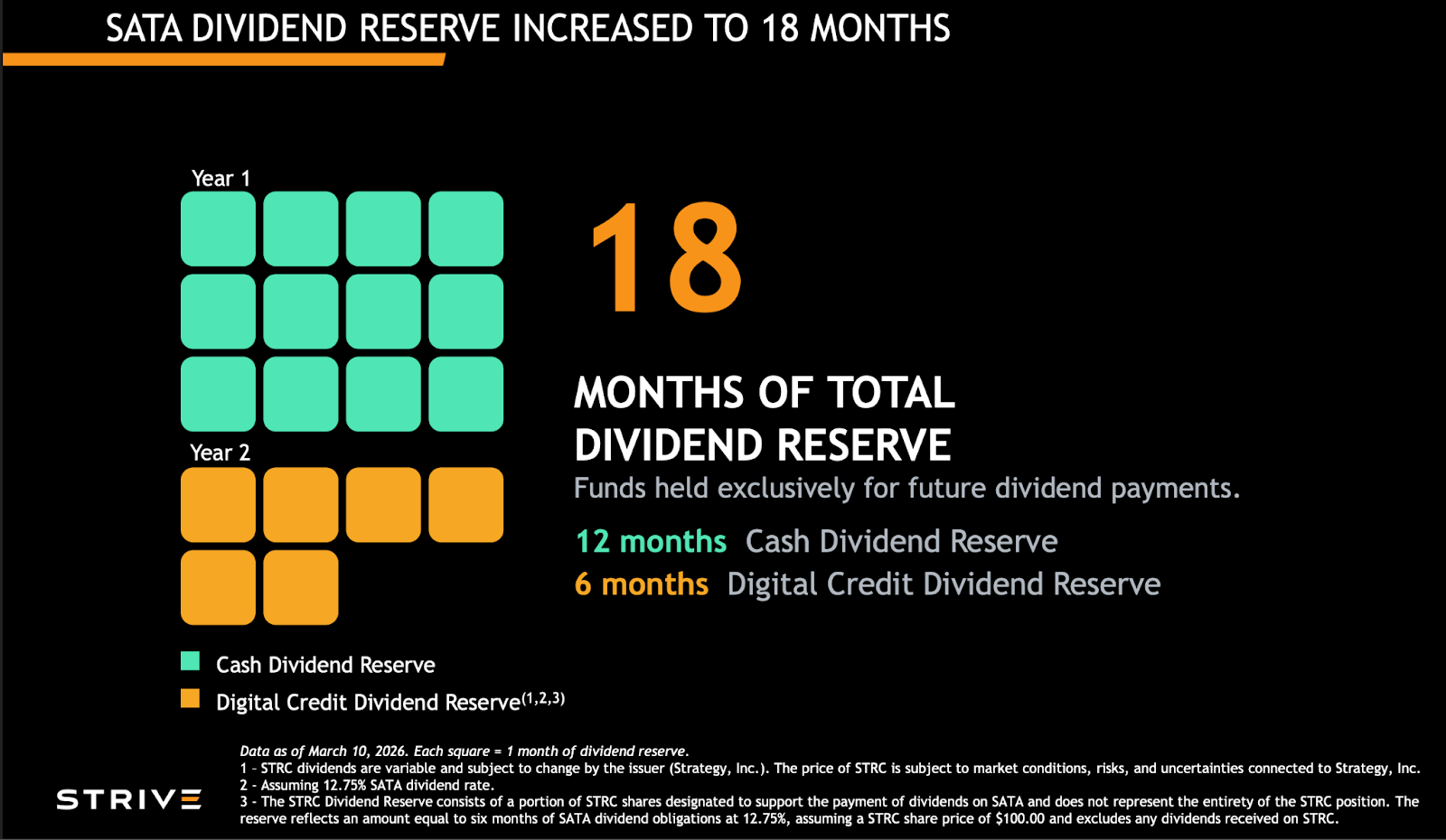

At launch, SATA had a 12-month cash dividend reserve. By March 2026, Strive said this had increased to 18 months of support, consisting of 12 months of cash and cash equivalents plus 6 months of STRC-based support, with the STRC portion calculated using a $100 STRC price assumption and excluding any STRC dividends received. As of March 9, 2026, Strive also reported $143.4 million of cash and cash equivalents, before noting that $50 million of that had subsequently been used to purchase STRC.

For institutional readers, the nuance is obvious: not all reserve support is equal. Cash is the strongest form of reserve. STRC support is still useful, but it is market-sensitive and depends on the value and behavior of another instrument. The key point, however, is that the reserve architecture is visibly improving. SATA is no longer being presented as just a high-yield preferred. It is being supported by a layered system of cash, marketable securities, and a large liquid reserve asset base.

For ordinary investors, the simple takeaway is that SATA’s income stream is not floating unsupported. It sits within a capital stack that management is actively building out to make the payout look more durable.

Why STRC makes SATA stronger

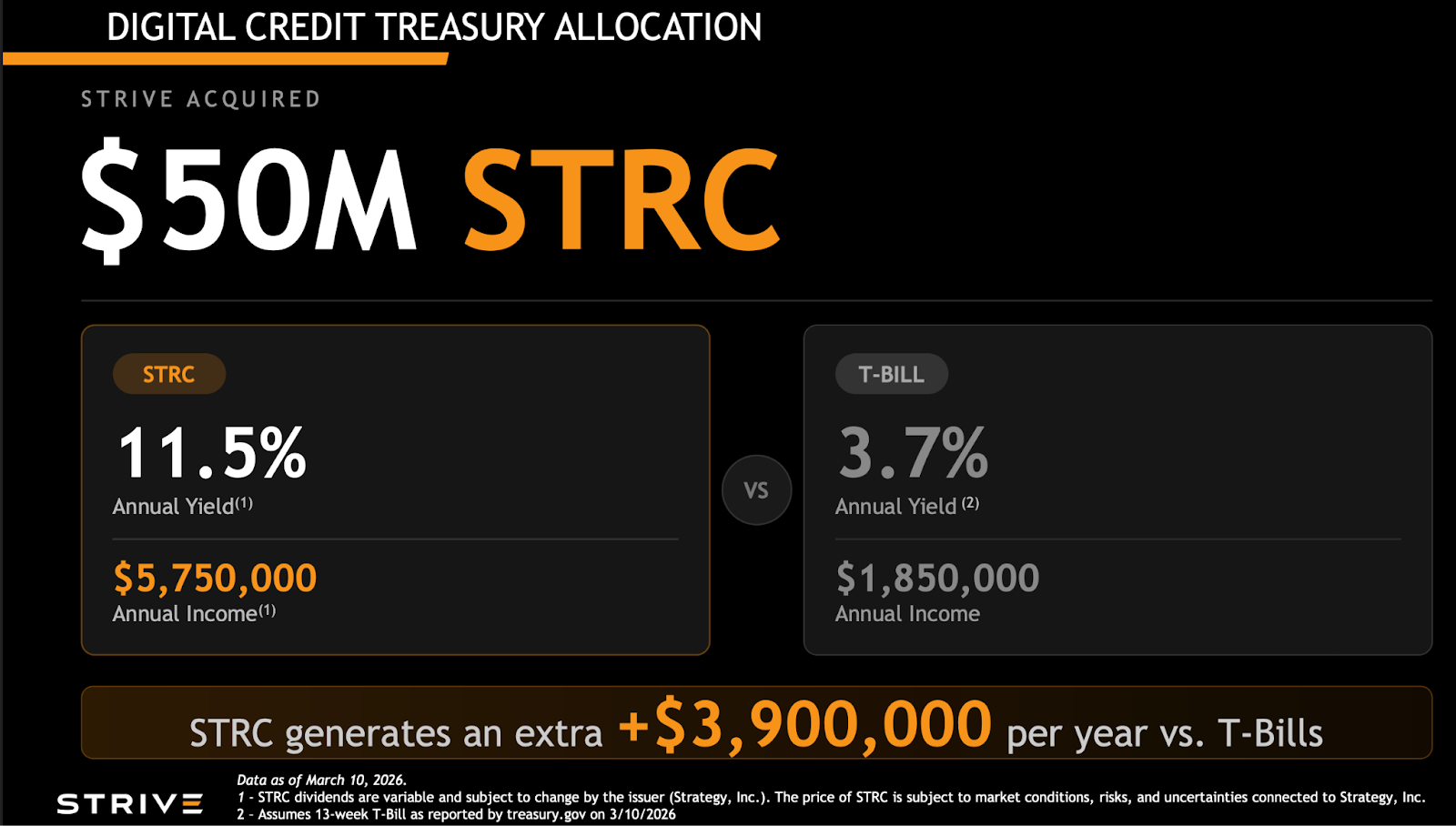

The March update introduced a new element: Strive had purchased $50 million, or 500,000 shares, of STRC. The company framed STRC as a higher-yielding, liquid digital-credit instrument and explicitly positioned part of that holding as support for SATA’s reserve structure.

This matters for two reasons.

First, STRC potentially improves the efficiency of Strive’s treasury capital. The March deck compared STRC with 13-week T-bills and presented STRC as generating materially more annual income under then-current assumptions. That comparison is promotional, and it comes with important caveats, but the broader idea is rational: if management can hold a liquid income-producing instrument rather than idle low-yield cash, the support behind SATA becomes more productive.

Second, STRC helps turn SATA from a one-dimensional yield product into part of a broader digital credit treasury architecture. This is where the story becomes more interesting than a simple preferred stock narrative. Strive is not just raising capital it is building a layered structure where one yield-bearing instrument can support another, while both sit inside a broader Bitcoin-heavy balance sheet.

That is a sophisticated institutional move. It signals that management is thinking not merely in terms of financing events, but in terms of portfolio construction.

Bitcoin is not the collateral, but it is the engine

The most misunderstood part of SATA is probably the role of Bitcoin.

Critics will point out, correctly, that SATA is not collateralized by Bitcoin. The company’s materials say so explicitly. SATA holders do not own the Bitcoin and do not have a direct lien on it.

But that does not mean Bitcoin is peripheral. On the contrary, Bitcoin is the economic engine of the entire architecture.

By January 28, 2026, Strive reported that it had acquired 333.89 BTC, bringing total holdings to 13,131.82 BTC. By the March 11 update, based on March 9 data, it disclosed a further 179 BTC purchase, lifting holdings to approximately 13,311 BTC. Incorporating your updated March 17 figure of 317 BTC, Strive’s Bitcoin treasury stands at roughly 13,627 BTC as of March 27, 2026. The directional takeaway is clear: Strive continues to expand the reserve asset base underpinning SATA, strengthening the balance-sheet foundation behind the preferred structure.

Why does that matter? Because SATA’s support improves as the asset base supporting the company grows. Bitcoin functions here less like a speculative side bet and more like a balance-sheet amplifier. If Strive continues to accumulate Bitcoin while keeping the preferred liability structure disciplined, SATA may become increasingly well-supported relative to its annual dividend burden.

That is the conceptual breakthrough. Most income products are backed by cash flows that slowly depreciate or remain static. SATA is being backed, economically, by an asset strategy that management believes can appreciate over time. That does not eliminate volatility. It does create the possibility of an income instrument whose support base grows rather than erodes.

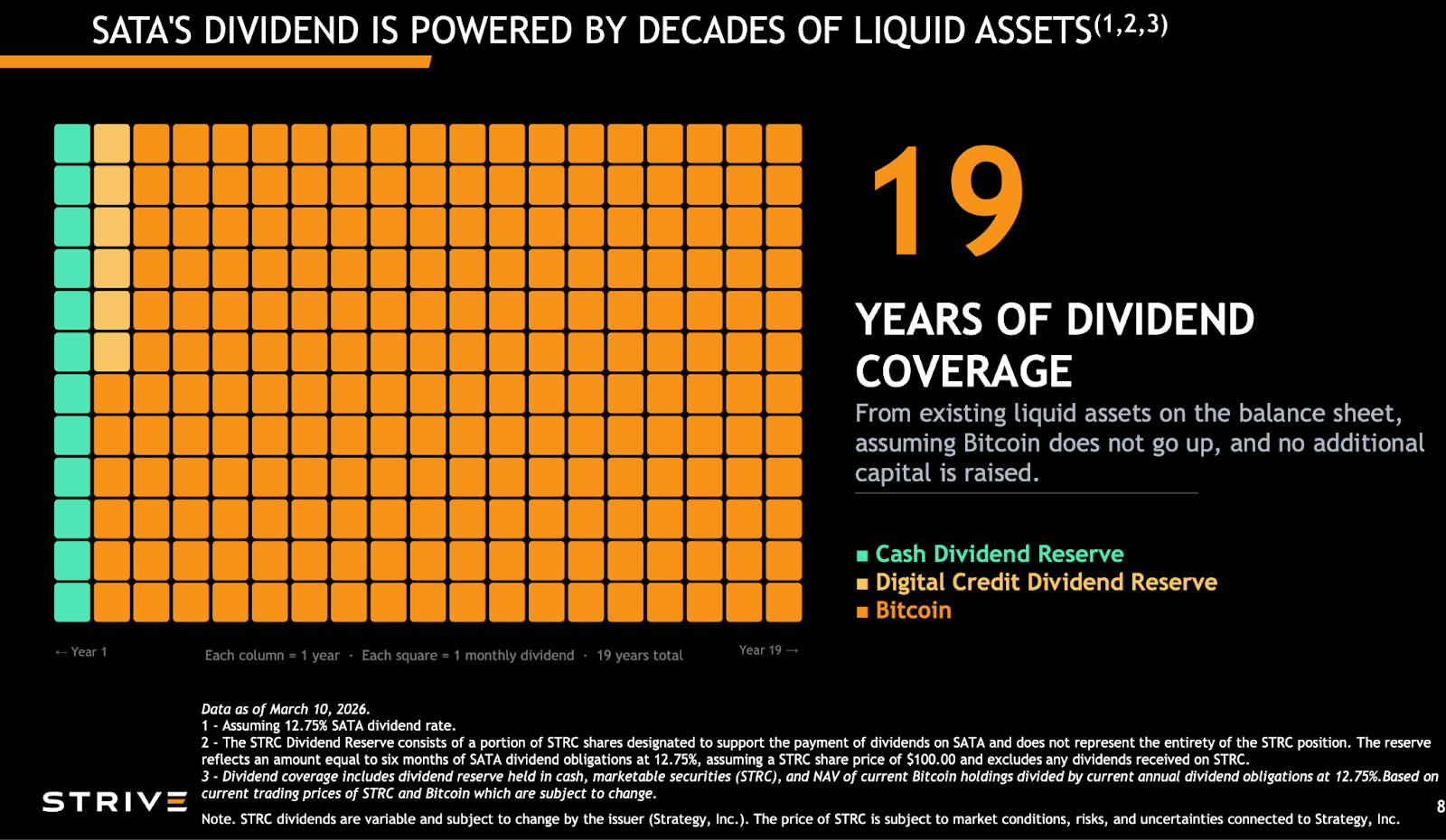

The “19 years of coverage” claim should be read correctly

One of the headline figures in Strive’s March materials is that aggregate cash, STRC, and Bitcoin cover 19 years of SATA interest payments, or more than 19 years of dividend obligations under current assumptions. The company explains that this figure is calculated as the sum of cash reserves, marketable securities, and the NAV of current Bitcoin holdings, divided by annual SATA dividend obligations at the current 12.75% rate. It also notes that the figure depends on current trading prices of STRC and Bitcoin, both of which can change.

This is where a good analysis must be both bullish and disciplined.

The right way to read the 19-year figure is not as 19 years of hard cash sitting in escrow. It is a coverage concept, not a literal lockbox. It tells you that, at then-current market values, the resources associated with the company are large relative to the annual dividend burden of SATA.

That is still very important. A coverage ratio is not the same thing as a contractual reserve, but it is absolutely relevant in credit analysis. It tells you the liability is relatively small compared with the asset base standing behind the enterprise. For a preferred stock linked to a Bitcoin treasury strategy, that is exactly the kind of relationship investors want to see.

In other words, the number should not be taken naively, but neither should it be dismissed. Properly understood, it is directionally powerful.

Why SATA could matter far beyond Strive

The bullish case for SATA is not only about this one security. It is about what the security represents.

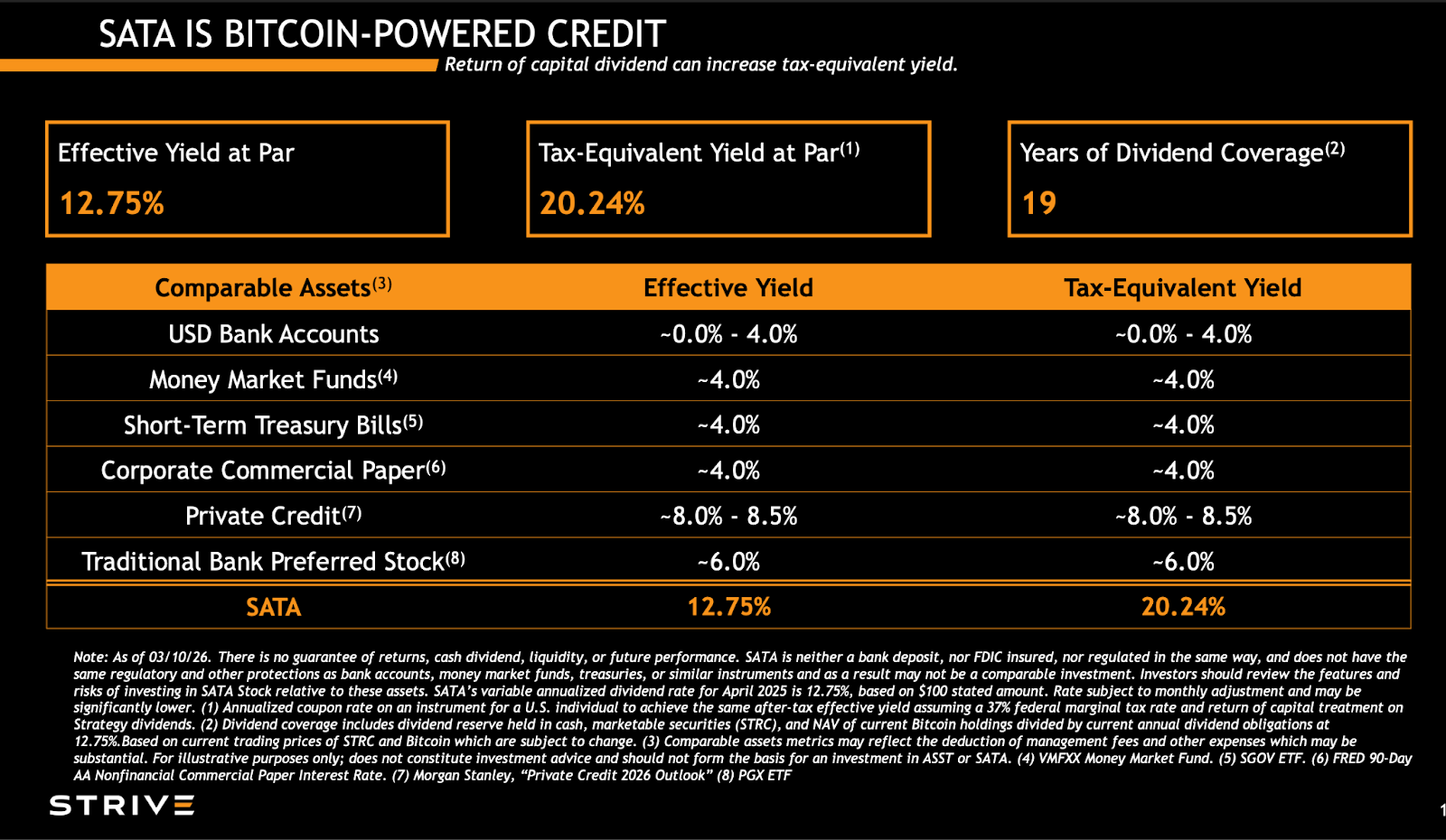

If Strive succeeds, SATA could become one of the first widely understood examples of Bitcoin-powered credit: an instrument that uses a Bitcoin-rich balance sheet to support a high-income, relatively stable preferred security for investors who want yield without taking pure common-equity risk. The company is already describing SATA in those terms, comparing it with bank deposits, money market funds, T-bills, private credit, and traditional bank preferreds, while highlighting a 12.75% effective yield at par and a 20.24% tax-equivalent yield under the assumptions shown in the deck.

Some of that presentation is naturally promotional. But the strategic idea is real. There is a growing class of investors who want exposure to the monetization of Bitcoin treasuries without simply buying common equity and accepting all the volatility that comes with it. SATA may be an answer to that need.

In that sense, the security is larger than its own terms. It is a live experiment in whether Bitcoin can support a new layer of institutional income products.

The risks are real, but they do not break the thesis

The most obvious risk is that dividends remain board-declared. SATA may be cumulative, but cumulative is not the same thing as guaranteed current payment. Another risk is that the support narrative depends significantly on Bitcoin prices. If Bitcoin falls sharply, coverage metrics weaken. A third risk is that the reserve structure is mixed quality: the first 12 months are framed as cash support, while the additional 6 months depend on STRC-related support and therefore involve more market sensitivity. There is also governance risk, because the structure is management-driven, and history shows management was willing to issue below par in January when it felt the strategic trade-off was worth it.

These are serious considerations. But they are better understood as underwriting variables than thesis destroyers.

The reason is that each of these risks is counterbalanced by visible structural improvements. The company cleaned up inherited debt. It unencumbered Bitcoin. It increased the dividend. It expanded reserve support. It tightened price guidance. It added STRC. It continued accumulating BTC. The trend line is constructive, and that matters.

The bottom line

SATA is not a traditional preferred stock, and that is exactly why it deserves attention.

It is a high-yield, monthly-paying, variable-rate perpetual preferred with a $100 stated amount, a cumulative dividend structure, and a management team that appears to be intentionally engineering the product toward near-par stability and institutional usability. Since January 2026, the case has improved materially: the balance sheet is cleaner, Bitcoin is unencumbered, the dividend rate is higher at 12.75%, the target range is tighter at $99–$101, the company says it will not issue below $100, reserve support has expanded to 18 months, and the company has tied the product to a broader asset base that it says covers more than 19 years of annual dividend obligations under then-current assumptions.

Add to that the documented Bitcoin accumulation of 333.89 BTC by January 28 and 179 BTC by the March update, plus March 17 addition of 327 BTC, and the direction of travel is clear: Strive is not simply maintaining SATA. It is trying to strengthen it, professionalize it, and turn it into a durable flagship product in Bitcoin-linked credit.

For investors willing to understand what it is and just as importantly, what it is not SATA may prove to be one of the most compelling new income instruments in the emerging market for digital-credit finance.

FOLLOW US ON:

X (Twitter), Youtube, Instagram, Linkedin

Access to these products and services is restricted to non-U.S. persons and may not be available in certain jurisdictions.