Metaplanet Is Buying Through the Bear Market

The strongest Bitcoin treasury stories are not written in bull markets.

Anyone can look smart buying Bitcoin when price action is rising, capital is easy, and sentiment is strong. The real test comes when the market softens, volatility cuts both ways, and investors start asking harder questions. Do treasury companies slow down? Do they become defensive? Do they wait for better visibility? Or do they keep building anyway?

Metaplanet’s latest results suggest it has chosen the last path.

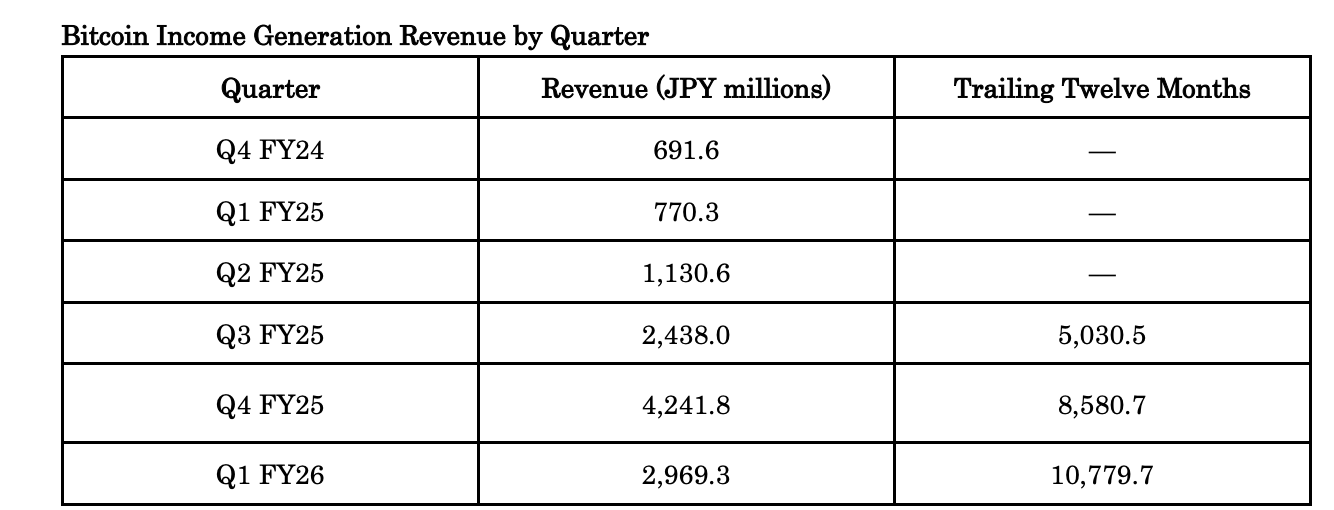

In the first quarter of fiscal 2026, the company generated JPY 2.969 billion of operating revenue from its Bitcoin Income Generation business, acquired 5,075 BTC during the quarter, and finished March with 40,177 BTC on its balance sheet. That combination matters on its own. But it matters even more in a softer Bitcoin environment, because it shows a company that is not merely holding conviction it is still converting that conviction into operating revenue, treasury expansion, and capital-markets relevance.

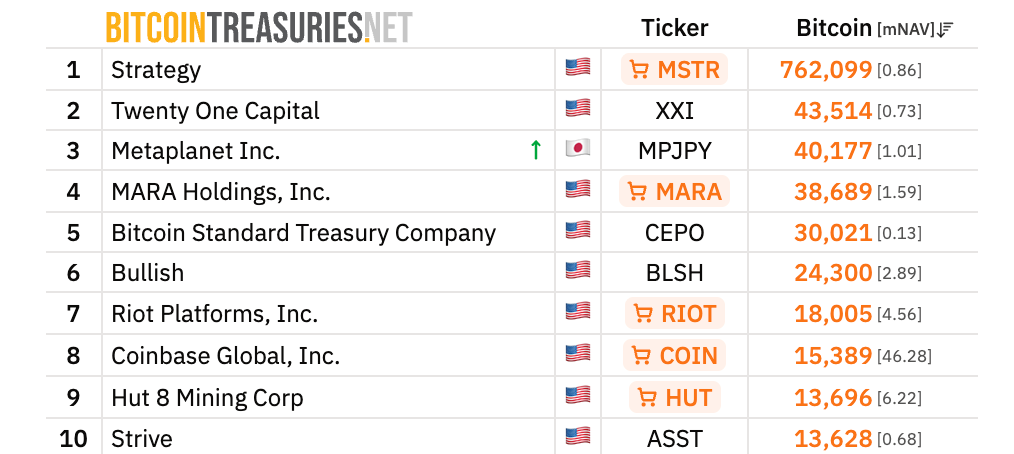

And that treasury expansion is no longer small enough to ignore. Based on the ranking you shared, Metaplanet has now moved into the third-largest Bitcoin treasury position among public companies, behind only Strategy and Twenty One Capital. That is not just a symbolic milestone. It changes how the company should be viewed. It is no longer simply an emerging Bitcoin proxy in Japan. It is becoming one of the defining public vehicles in the global Bitcoin treasury landscape.

That is the real significance of this moment. In a market where many participants become cautious when Bitcoin weakens, Metaplanet is still buying, still compounding, and still building a business line designed to generate cash flow around that accumulation strategy.

The most important thing Metaplanet proved this quarter

The central question around Bitcoin treasury companies has always been simple: can they become more than passive holders of a volatile asset?

Metaplanet’s Q1 update suggests the answer is increasingly yes.

The company’s Bitcoin Income Generation business is not presented as a side activity. It is now being described as an operating engine. According to the company, this business uses Bitcoin options to generate recurring operating revenue, while supporting Bitcoin accumulation over the medium to long term. The first-quarter result was JPY 2.969 billion. For context, full-year FY2025 revenue from the same business totaled JPY 8.581 billion, and the trailing twelve-month figure now stands at JPY 10.780 billion.

That trajectory is what makes the story increasingly credible.

A Bitcoin treasury strategy becomes far more powerful when it develops an internal source of cash generation. Without that, the model often depends too heavily on favorable equity issuance windows, rising Bitcoin prices, or investor tolerance for dilution. With it, the company begins to look more like an operating platform and less like a simple wrapper around a reserve asset.

That distinction becomes even more valuable in a BTC bear market or risk-off environment. When prices are weak, the companies that can still generate cash flow, still fund purchases, and still act decisively are the ones that separate themselves from the field.

Metaplanet appears to be doing exactly that.What the Bitcoin Income Generation business actually does

A lot of people hear “options” and assume the company is just speculating. That is not how Metaplanet describes it.

According to the company, the Bitcoin Income Generation business uses Bitcoin options, including collateral-secured option strategies, inside a dedicated income-generation portfolio. The company also states that this portfolio is operationally segregated from its long-term Bitcoin holdings. The long-term Bitcoin treasury is intended to be held on a perpetual basis and is not subjected to the same derivative exposure.

That separation is what makes the model more robust.

It means Metaplanet is trying to create two linked but distinct functions. One side is designed to produce recurring revenue. The other side is designed to hold Bitcoin for the long term. Over time, capital generated from the first side can help expand the second. But the long-term reserve itself is not meant to be constantly recycled back into options activity.

That is an intelligent structure, especially in a difficult BTC environment. It reduces the risk that the company’s long-term treasury thesis gets blurred into short-term trading behavior, while still allowing the company to monetize volatility and extract operating value from the market.

Why continued BTC buying in a weak market matters so much

The easy time to buy Bitcoin is when everyone already agrees with you.

The hard time is when Bitcoin is under pressure, confidence is mixed, and every purchase attracts more skepticism than applause. That is precisely why Metaplanet’s latest accumulation matters. The company did not pause. It did not retreat into observation mode. It bought 5,075 BTC in Q1 2026 and ended the quarter with 40,177 BTC in total holdings.

That kind of behavior sends a message.

It says the company is not treating Bitcoin accumulation as a momentum trade. It is treating it as treasury policy.

For institutions, that is a meaningful distinction. Treasury strategies are supposed to be durable, repeatable, and disciplined across cycles. If a company only accumulates aggressively in bullish conditions, then what it really has is opportunism, not strategy. But if it keeps accumulating while conditions are less forgiving, investors can begin to view the model as structurally intentional.

That is one reason Metaplanet’s move to the No. 3 position is so important. It is not merely that the company now owns more Bitcoin. It is that it appears to have advanced into that position while the market backdrop was less supportive than an outright mania phase. In that context, scale means more.

The rise to the third-largest Bitcoin treasury company changes the narrative

Rankings matter in capital markets.

They matter because markets organize attention around relative scale. The jump from being “one of many Bitcoin treasury companies” to being the third-largest public Bitcoin holder changes the category in which Metaplanet is discussed. It becomes more visible, more comparable, and more institutionally relevant.

The ranking you provided shows Metaplanet at 40,177 BTC, ahead of names such as MARA, Bitcoin Standard Treasury Company, Bullish, Riot, Coinbase, Hut 8, and Strive. That is an extraordinary repositioning in a relatively short period. It places the company firmly inside the top tier of global public Bitcoin treasury names.

That matters because treasury leadership can create its own momentum.

The larger the treasury becomes, the easier it is to attract investor attention. The more investor attention the company receives, the more effective its capital-markets positioning can become. And the more effective its financing platform becomes, the easier it can be to continue compounding the treasury. That kind of reinforcing loop is often how leaders emerge in new financial categories.

This is why the third-largest ranking is not just a headline. It is a signal that Metaplanet is moving from participant to category leader.

The company is still growing, even after dilution is considered

Another encouraging feature of the disclosure is the continued emphasis on BTC Yield, BTC Gain, and BTC ¥ Gain.

For Q1 FY2026, Metaplanet reported BTC Yield of 2.8%, BTC Gain of 876, and BTC ¥ Gain of JPY 9.293 billion. These metrics are designed to show whether Bitcoin accumulation is still accretive to shareholders on a diluted-share basis.

That 2.8% figure is lower than earlier breakout phases, but that is exactly what makes it credible. Metaplanet is already much larger now. Compounding at scale is inherently harder than compounding from a small base. The fact that the company is still reporting positive BTC Yield while expanding to 40,177 BTC suggests the strategy remains productive even after substantial treasury growth and capital-markets activity.

The company is also careful to note the limitations of these KPIs. They do not fully account for senior claims, debt, or every aspect of economic performance. That honesty strengthens the presentation. It signals a company that is trying to communicate like a serious capital allocator rather than a mere promoter.

Why the commendable part of the story is not just growth, but growth under pressure

Anyone can describe rising numbers.

The more meaningful question is what kind of environment those numbers were achieved in.

That is why the tone of this quarter should be read as one of resilience. Metaplanet is not merely reporting expansion. It is reporting expansion while the broader Bitcoin backdrop is challenging enough that continued buying itself sends a message. The company is still generating revenue from Bitcoin-linked market activity. It is still lowering the effective economics of treasury accumulation. It is still scaling the treasury. And it has now climbed into the third-largest public Bitcoin treasury position.

That combination deserves recognition.

Because the real signal here is not just that Metaplanet is growing. It is that Metaplanet is growing through conditions that might have caused a less committed or less well-designed treasury strategy to slow down.

That is what makes the quarter impressive.

Final conclusion

Metaplanet’s Q1 FY2026 update is powerful not just because the numbers are large, but because of when and how those numbers were achieved.

In a market environment where a weaker Bitcoin backdrop could easily have led to caution, the company kept buying. It generated JPY 2.969 billion of operating revenue from its Bitcoin Income Generation business, acquired 5,075 BTC in the quarter, and ended March with 40,177 BTC on the balance sheet.

That performance has now pushed Metaplanet into the position of the third-largest public Bitcoin treasury company based on the ranking you shared. More importantly, it shows that the company is not relying on a single lever. It is building a more complete Bitcoin capital model: one that combines treasury accumulation, recurring income generation, and increasingly sophisticated capital-markets execution.

That is what makes the story compelling.

Metaplanet is not waiting for a perfect market to keep building. It is building anyway. And in Bitcoin finance, that is often what separates the companies that merely participate from the ones that lead.

FOLLOW US ON:

X (Twitter), Youtube, Instagram, Linkedin

Access to these products and services is restricted to non-U.S. persons and may not be available in certain jurisdictions.